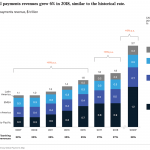

According to McKinsey´s September 2019 Report, the payments sector generated $1.9 trillion of revenue in 2018, growing 6% compared to the year before, surpassing the GDP growth rate of regions like North America, and Asia-Pacific (source). It’s no surprise that even the non-financial institutions want a slice of this cake.

Source: McKinsey Global Payments Report 2019

McKinsey’s September 2019 report also shows that the payment companies in Asia-Pacific took the lead in payment revenues, and generated more revenue than EMEA, North America, and Latin America combined. As expected, China single-handedly took the lead in the Asia-Pacific region’s 2018 share with a $605 billion revenue.

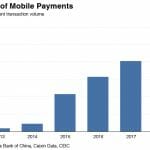

Source: China’s Mobile Payment Transaction Volume Hits $41.51 Trillion in 2018

Mobile payments occupy a significant portion of the Chinese payments market. Proving the world that cashless society goals are actually achievable, the Chinese payment market has been a global front-runner in the mobile payment sphere, with 86% mobile payment penetration rate (source) in the country. Average Chinese customers use cash in less than 20% percent of monthly transactions, and 73% of customers claim to be able to manage to finance a whole month with less than EUR 12 in cash (100 RMB) (source). Research clearly demonstrates that the Chinese mobile payment market didn’t let us down in 2018 as well, transaction volumes reaching the peak with $41.51 trillion, which is five times more than five years ago and are expected to soar in the next years (source).

Source: PwC Global Consumer Insights Survey 2019

90% of the mobile payments sphere in China is dominated by two companies, AliPay (Alibaba) and WeChatPay (Tencent), which are actually spin offs of (initially non-financial) technology companies. These companies used their scaling power in the retail and social spheres to fire a financial innovation, integrating finance into everyday scenarios. Currently, Alipay and Tencent handle more payments in one month than PayPal handles in one year. Western financial institutions still try to conjecture the secret behind this dual success, and why applying the same methods hasn’t achieved the same level of success.

They say it takes a village to raise a child and, in this case, it took an entire ecosystem to drive the local payment innovation:

- Service Culture: First of all, the lack of service culture in some western regions has proven to leave the regional financial institutions behind. Both AliPay and WeChatPay payment technologies were initially created as add-on systems, seamlessly integrated into other services, aiming to improve the user experience. Therefore, the companies were able to grow organically together with the offered services.

- Correct Innovation Strategy: While banks were still at point zero with their digital transformation strategies, Alipay and WeChat were already experimenting with payment technologies. The experimentation at the early stages of their operations allowed these companies to figure out the needs of the local user base and develop accordingly. Observing the momentum these companies gained, Western banks tried to achieve the same results with copycat methods, stretching out legacy technologies, which didn’t meet the expectations. As we all learned, innovation cannot be copied; it has to be integrated.

- Tailoring the System According to the Market Needs: Banks were historically underdeveloped in China, and the solutions they offered didn’t fulfill the needs of the ecosystem. Additionally, Chinese customers do not have a history of owning and using credit cards. Therefore, AliPay and WeChatPay’s solutions that simplify the end-to-end payment experience changed the system as a whole, which ended up raising the bar for the customers.

- Low Technology Costs: The majority of (Western) banks still use legacy payment technologies and for such financial institutions, changing these structures and integrating new systems is costly and time-consuming. New companies that start their offerings with a brand-new payment system have a competitive advantage in terms of operational costs and hence the successful payment integration results in China. As a result, catching up with the new wave of payment schemes were easier said than done.

- Simplifying Partner Processes and Reducing Partner Costs: Quid pro quo – a favour for a favour. Merchants in China enjoyed, and thus, fanatically supported the use of digital payments for more efficient and cheaper business operations. Offering digital payments didn’t only decrease the costs, but also reduced the chances of fraud and enabled SMEs to expand their services based on multi-channel and omni-payment channel strategies.

- Demographics: During the development phase, demographics also served in the best interest of these two companies. The quick adaptation of mobile payments in the region can also be interpreted as a result of the younger population and particularly tech-savvy middle class.

- External Support: Up until recently (source), the Chinese central bank and the government have been actively promoting mobile payments in the belief that these systems have the potential to increase productivity in the economy as a whole and therefore, it would be impossible to disregard the role of external support in the adaptation process. Combined with a rather open regulatory environment, this support seems to have positively affected the amount and volume of the transactions.

- Interoperability: The fact that users do not have to choose one service over another (except the Taobao network) makes it easier for both merchants and the customers. As participants of this interoperable network, both AliPay and WeChat Pay ensure fair competition which tends to grow the market as a whole.

- Sticky Services: Retention is a big portion of growth, and both AliPay and WeChatPay ensure retention by making their services sticky, both locally and internationally. In addition to offering a variety of services, these companies also follow their customers everywhere through their partnerships in foreign countries. At the end of the day, once a customer gets hooked, there seems to be little room for competitors to steal that user, as the company follows a strategy of shadowing users everywhere, offering the same scope of services in other continents and cooperating with local service points.

Although globally, the majority of the banks are struggling to move into profit in the payments sphere (source), these two Chinese payment companies have been enjoying a big spread of margins, without the interference of any western company – though this is now about to change. PayPal, the pioneer of electronic payments, is preparing to be the first payments company that will enter the Chinese PayTech market through the acquisition of the controlling shares of a local company. The People’s Bank of China has given a greenlight to PayPal’s acquisition of the majority stakes of GoPay (Guofubao Information Technology Co., Ltd.) on 30.09.2019 (source). GoPay is a small-scale tech company that is already granted licenses for online, cross-border, and mobile payment services along with pre-paid card issuance and acceptance services (source).

Following the approval from the regulator, PayPal released the following statement:

“The People’s Bank of China has approved PayPal Information Technologies Co., Ltd.’s acquisition of a 70% equity interest in Guofubao Information Technology Co. (GoPay), Ltd., a holder of a payment business license in China. We are honored to become the first foreign payment platform to be licensed to provide online payment services in China. We look forward to partnering with China’s financial institutions and technology platforms, providing a more comprehensive set of payment solutions to businesses and consumers, both in China and globally. The transaction is expected to close in the fourth quarter of 2019 and is subject to customary closing conditions.”

PayPal’s acquisition immediately triggered speculations about the company’s timing to enter the Chinese market and the continuity. Indeed, there are already two consolidated and preferred companies existing; however, the market is predicted to grow even more in the future. The Chinese mobile payment market is expected to evolve into a $96.73 trillion market by 2023 (source). Furthermore, both AliPay and WeChat Pay require a Chinese bank account for registration and adding a foreign bank account to these wallets isn’t so easy. This policy hasn’t been creating a user-friendly traveling experience for tourists, especially in regions with no cash policy. PayPal’s existence might be able to solve this issue. All in all, the existence of either of the two local payment giants do not seem to threaten each other due to different use cases and interoperability and thus there might even be room for a third one.

On a different note, only since 2017, the Chinese market is welcoming foreign payment companies. PayPal is definitely not the first western payment company that is trying to enter the market but the first one that was granted with full access. The Chinese government’s mission for diversifying the market hasn’t been too fast, but now, we can see the light at the end of the tunnel. As a Chinese proverb says, “Be not afraid to go slowly, be afraid only to stand still”. Upcoming quarters will show how PayPal CEO Dan Schulman’s “never stand still” mantra (source) pays off in penetrating the Chinese market.

Author: Sebnem Elif Kocaoglu Ulbrich, Fintech and Payment Expert