Lasting change

When the pandemic erupted, one could have entertained the notion that changes in consumer behaviour and the adaptations required from the business community might be fleeting.

As the harsh reality of vaccine logistics & the challenges posed by new variants of the virus settle in, and societies worldwide continue to hunker down in order to avoid worst-case-scenarios from a healthcare perspective, it becomes increasingly clear that changes to the way people transact are here to stay.

It is no coincidence that Amazon just posted a 44% YoY increase in quarterly sales, reaching a breath-taking $125bn and $386bn for the full year 2020 (a 38% increase compared to 2019).

While Amazon remains the “800 pound e-commerce gorilla” of the Western Hemisphere, the trend towards online sales as well as mobile payments – and greater integration of the two – provides ample opportunity for a large number of players to carve out their respective niches.

Constructive interference

Reports of belief-defying “rogue waves” are documented dating back to at least the 19th century, yet it took quite a bit of insight into the underlying physics to cement their acceptance as a naturally occurring phenomenon. Part of the “knowledge bottleneck” in terms of driving acceptance of these “freak” events was the fact that very few ocean-faring vessels and crews could survive such a force of nature. Survivors were mocked for what others viewed as exaggerated claims.

Today we know that “rogue waves” occur rather frequently, and ubiquitously, in nature, spurred on by a physical phenomenon known as “constructive interference”, defined as follows:

“the maxima of two waves add together (the two waves are in phase), so that the amplitude of the resulting wave is equal to the sum of the individual amplitudes”.

Here I will argue that the explosion in e-commerce and mobile payments is the result of “constructive interference”, resulting from a combination of pre-COVID, organic dynamics in consumer behaviour driven by technological progress, as well as the “big push” that was triggered by the pandemic and the resulting lockdowns and restrictions.

Case in point, Amazon’s rise has been inexorable and it surpassed America’s largest brick-and-mortar retailer, Walmart, in terms of valuation back in 2015:

It is Amazon’s principled reinvestment of its – parabolically growing – revenues into worldwide infrastructure and promising new business segments such as AWS that positioned the tech behemoth to take full advantage of COVID-induced changes when they struck.

Unless regulators decide to poke some holes into Amazon’s mighty hull, there is no reason to think that the company will stop riding the e-commerce rogue wave anytime soon.

Embedded everything

Integration could well be the keyword for financial services going forward.

A white paper by EPA EU member tribe “surveyed over 125 fintech executives to find out how they thought the industry would change in the next 10 years”, and “a key theme for many was the idea of payments, lending and trading being invisible, seamless, and integrated—and following this, finance in general doing the same.”

Featured in the same publication, Matthew Harris of BainCapital Ventures describes this ongoing convergence as a function of leveraging existing revenue streams to create new offerings all the while minimising risk. Citing e-commerce platform Shopify, he notes that 59% of the company’s 2019 in fact came from its payments activity.

The Luxembourg ecosystem has taken notice.

LHoFT member Joompay recently announced the launch of a EU-wide P2P payments app “to take on Transferwise and others” after obtaining its EMI license in Luxembourg in 2020. TechCrunch reminds us Joompay was started by the co-founders of the successful e-commerce marketplace Joom, a testimony to the dynamic highlighted by Bain Capital.

Furthermore, the fact that this P2P payments service is being launched into an already crowded field suggests that entrepreneurs see continued opportunity in the mobile payments space despite the competition.

The realization that seamless integration is a potential win-win for a multitude of participants is definitely resonating in the industry.

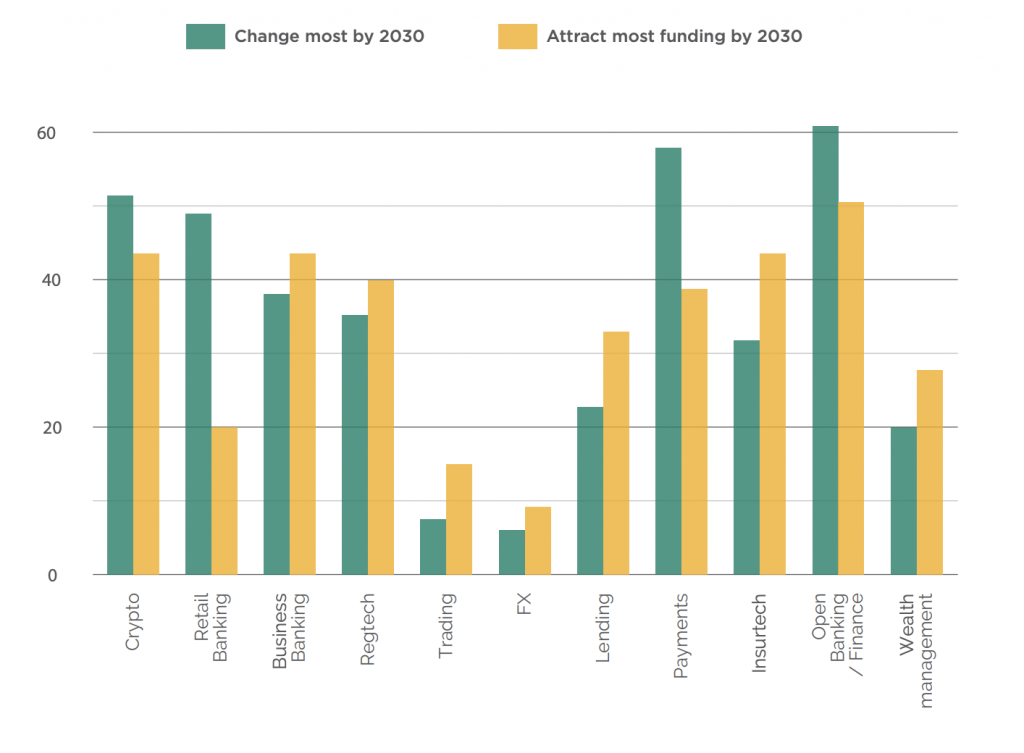

The payments space is widely expected to see significant change over the coming years.

Graph source: Tribe survey

Presenting at the recent Paperjam 10×6 Sales & Marketing event, Alicia Brun of Payconiq emphasised this by highlighting the importance of the “omnichannel” strategy in the payments sector. She cites studies showing that 20% of buyers abandon their purchases due to inconveniences and concludes that mobile payment systems are in many ways the “gold standard” for both online and offline payments.

In another noteworthy development, EPA EU member Banking Circle & HIPS payment announced a partnership to allow for instant currency conversion, stating that “the two companies will leverage each other’s technology to bypass old, bureaucratic and expensive systems. Instead of sending expensive international wire transfers, Hips can now use Banking Circle’s infrastructure to send payouts to merchants quickly, at low cost, compliantly and securely.”

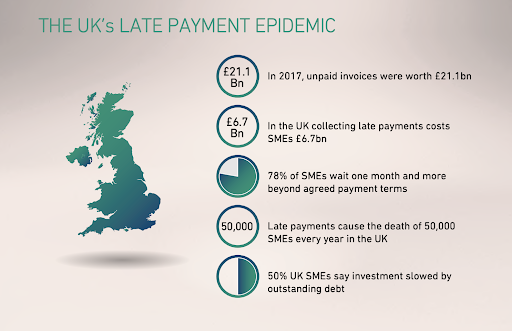

As shown below, late payments are a significant issue for SMEs in particular, and innovative, dynamic players such as Banking Circle contribute to financial inclusion via their more convenient and/or more effective offerings.

Image Source: Banking Circle

Be prepared or be scared

With all of the above in mind, it should be clear that “business as usual” is not coming back. As would be expected from a foundation tasked to promote the development of the fintech ecosystem, we often preach that incumbents must accelerate the pace of innovation and collaboration with innovative newcomers.

Perhaps the same sentiment, coming from the head of one of the world’s largest banks, carries even more “oomph”: no other than JP Morgan’s Jamie Dimon was recently heard telling analysts that incumbents should be “scared shitless” by fintech rivals, as is being reported here and in many more media outlets. The venerated banking titan furthermore explained that he expects the payments space to be the “main battleground” for the industry over the coming decade.

Those are clear statements, and while we like to view the dynamic between incumbents and innovators in less martial terms, we could certainly agree that a lack of preparation with regard to the new reality in business and finance is no longer a viable option.

Author: Jérôme Verony – LHoFT Research and Strategy Associate