On the 16th of June we were fortunate enough to host with Luxembourg For Finance representatives from across Luxembourg’s Asset Management and financial services industry, as a part of our International Showcase series of webinars. The recording is available to watch on our Youtube channel, and the slides may be downloaded here, and we’ve also transcribed the full talk and Q&A section here.

Antony Martini, Engagement Manager, LHoFT Foundation

Welcome everyone to the first international showcase, of a series of four focusing today on the asset management industry in Luxembourg.

Let me introduce our speakers:

Robert Jarvis, adviser at Luxembourg For Finance. Luxembourg for Finance (LFF) is the Agency for the Development of the Financial Centre.

Francois Drazdik from ALFI, the Association of the Luxembourg Fund Industry. ALFI represents the face and voice of the Luxembourg asset management and investment fund community.

Nicolas Gérard is Managing Director of the State Street Bank in Luxembourg.

On the moderator side, we have our co-host and colleague Alex Panican, Head of Partnerships, and Ecosystem development at the LHoFT.

Alex Panican, Head of Partnerships and Ecosystem, LHoFT Foundation

Thank you so much Antony for the introduction.

So due to the COVID-19 problem that we all faced, most of our conferences, abroad and nationally, have been canceled. So, we are bombarded with thousands of emails from Fintech asking us questions about the financial industry, about Luxembourg, how it is to work with the financial actors, how to set up a business. That is why we have decided, with Luxembourg for Finance and some associations from the financial industry, to set up a series of webinars to showcase the Luxembourg financial industry to the world, and to answer your questions.

So, without any further ado, let’s start with our first experts. Robert, please, can you introduce the asset management industry in Luxembourg?

Robert Jarvis, adviser at Luxembourg For Finance

Thank you very much.

What I do is that I help Fintechs to understand what Luxembourg can offer them. I’ll go over what made Luxembourg one of the leading financial centres in the European Union. We are often ranked as number two or number three. Now maybe post Brexit we climb up the ranks a little bit, but we’re not happy about Brexit.

Luxembourg is at the heart of the European Union, founding country of the European Union, located between Belgium, France, and Germany. The European aspect shapes our industry. We are of course home to Schengen, the reason why you can travel around the European Union without a passport but it’s also the reason why you can do business from one location to another. What this has created is European spirit.

We are one tolerant nation and we have three official languages: French, German and Luxembourgish, and the business language is English. On average Luxembourgish citizens speak over three languages, almost four languages, which is an important part of what we can do as a financial sector. It’s a very cosmopolitan country with around 50% of the population as foreigners, and that again helps us in our financial services.

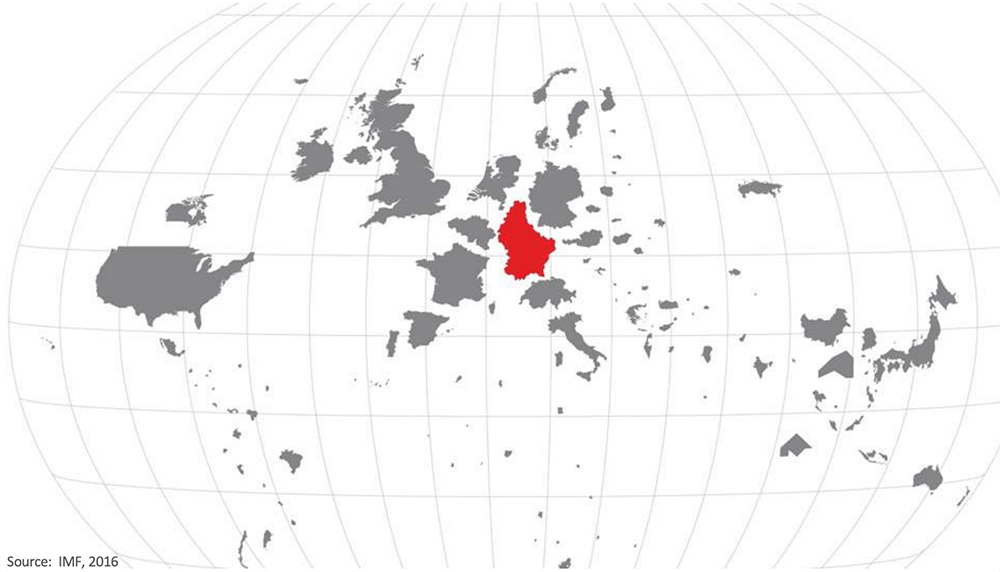

This is a map by the IMF from 2016, but even if it was updated today, it would look pretty similar. It’s a world map that reshapes the size of each country according to the size of their cross border financial activities. So that is cross border finance. As you can see, Luxembourg is bigger than France, bigger than Germany, bigger than Japan and even bigger than China. Only perhaps the US, bit of the UK would be bigger than Luxembourg. That’s what we do. We do financial services across borders.

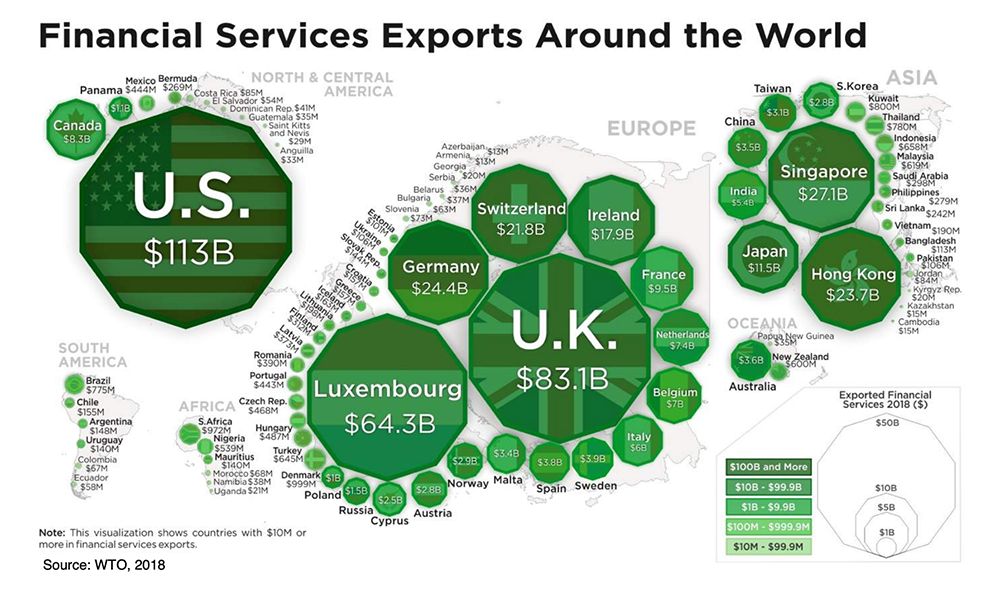

This next slide is the same kind of map. But this is focusing just on exports, not on imports. And as you can see, Luxembourg, is the third biggest financial services exporter in the world. And why can we do this? Because of the European Single Market and that allows cross border trade. Luxembourg sits there in between other countries, and allows you to trade with all of the 500 + million consumers, all of the financial institutions, and even beyond. Luxembourg acts as a hub for businesses and for asset managers and investment funds to do this cross-border activity. And at the same time, it offers this in a country that is economically stable, politically stable, and socially stable.

Now what our financial center specializes in is in four key industries. So that’s the asset management industry, banking, insurance and capital markets. I’m going to briefly cover each of them on the next slide.

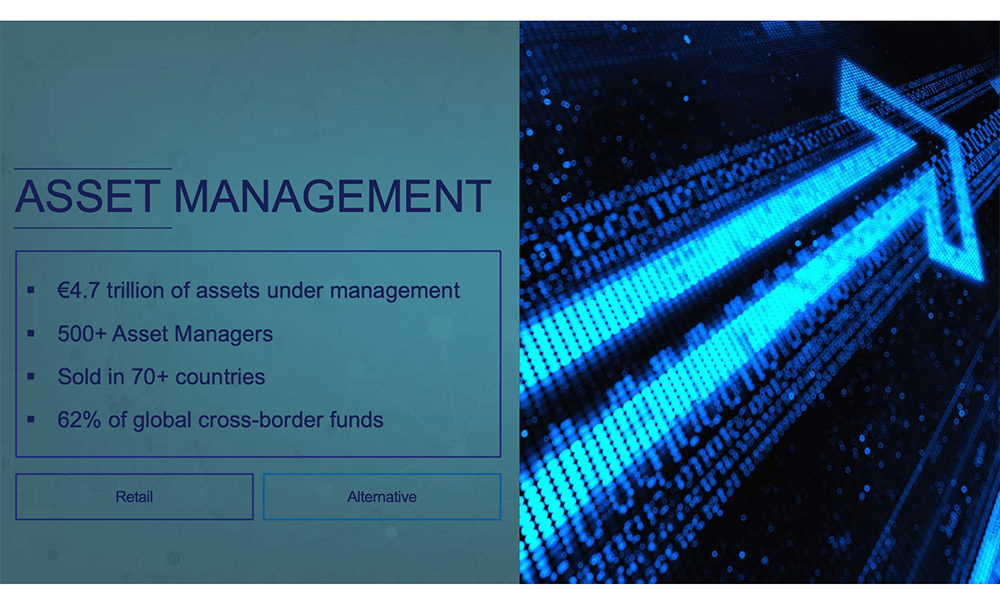

So we have around 4.7 trillion euros of assets under management in Luxembourg investment vehicles. And these investments are collected by many people in the world, who give their money to another manager who invests it in the long term. Luxembourg collects this money and distributes this money in over 70 different countries. So that is what Luxembourg has become. Much like you would buy a German car for its reliability, you buy Luxembourg investment products as well regulated, and trusted. It makes sense for an asset manager to set up a vehicle in one location and capture investments from all over the world and then to invest into projects, thereby again, helping the real economy.

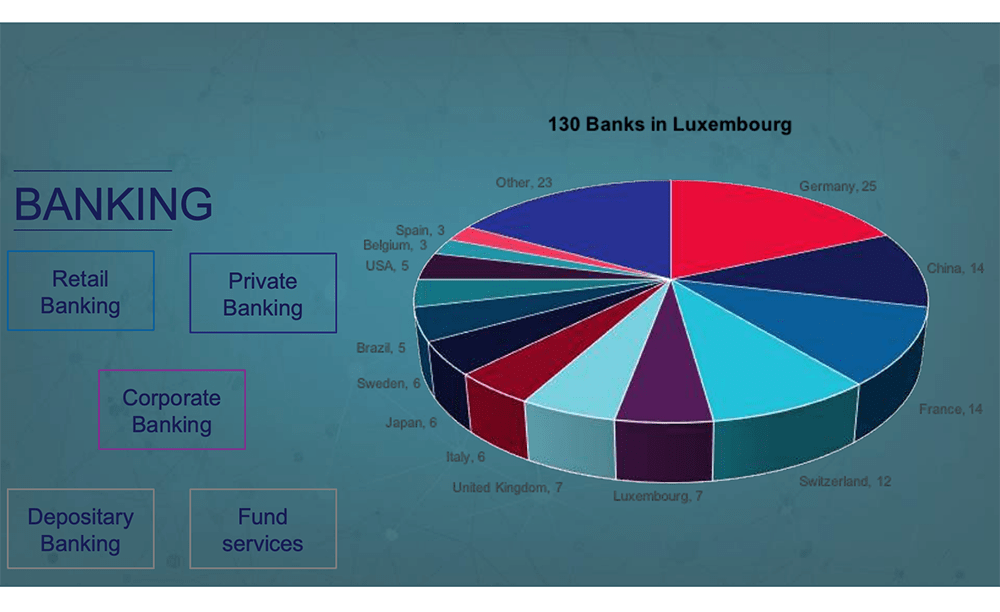

There are around 500 asset managers in Luxembourg, and we’re the global leader in cross border investment funds so that for Fintechs means clients: Asset Management clients, banking clients, insurance clients, lots of international business. The fund industry needs a lot of banking as well, and we have around 130 banks in Luxembourg.

One of the largest industries in Luxembourg is the fund service, because everybody thinks that asset management is simply about investing, but in a typical Asset Management value chain, only around 10% of the workforce is an investment. All of the rest is behind the scenes. And the more countries you sell products into, the more services are required, because if you imagine one investment from the product being sold into 70 jurisdictions, that needs to be translated, it needs to be applicable to the regulations, be it in Hong Kong, be it Chile be it in Italy. So there’s a lot of services behind the scenes in the asset management industry. We also have a burgeoning insurance industry where again, we focus on cross border insurance. Same with our capital markets, we focus on cross border activities where we have international debt listed by governments, as well as by large international corporations that use Luxembourg as a platform to list their products unable to gain visibility internationally.

We’re an international center. You can see all of the big names from Europe, all of the big names from America, South America, bit less Middle East and Africa was a bit less, but a very large Asian focus. We have the big Chinese banks that do business from Luxembourg, as well as the Japanese banks and asset managers, but also a lot of the Fintechs. If you look closely, you’ll see Alipay, you’ll see Rakuten, etc. from Asia. And this is what Luxembourg allows.

Multilingualism is an important part for many of these international financial institutions that come to Luxembourg, because here they find a stable country to do business internationally. And they find the workforce that allows them to operate in one location, that speaks Italian, that speaks Chinese, that speaks English and that speaks German. So, it makes sense for businesses to set up their operations here and use it as a hub for the European Union. And finally, perhaps, the asset management industry in Luxembourg is probably the most important sector of the financial industry. It employs around 15,000 people, and the entire financial sector employs around 50,000 people. And it contributes greatly to the GDP as well to the tax revenues of Luxembourg. Because every single investment fund pays a “taxe d’abonnement” which helps the government itself to finance projects and finance the economy in Luxembourg.

Now, pass it over to Francois Drazdik. From ALFI, which is the Luxembourgish fund industry association.

François Drazdik, ALFI

Good afternoon, everybody.

The ALFI association was created back in 1988. We are a not-for-profit organization supported exclusively by our members, which are different service providers in the investment fund industry, so we do not get any subsidy from the government in Luxembourg. We have more than 1500 members, and we are a representative body for the Luxembourg investment fund community that is composed of Luxembourg domiciled investment funds, asset managers at the national companies, services providers, and associate members based in other pan-jurisdictions.

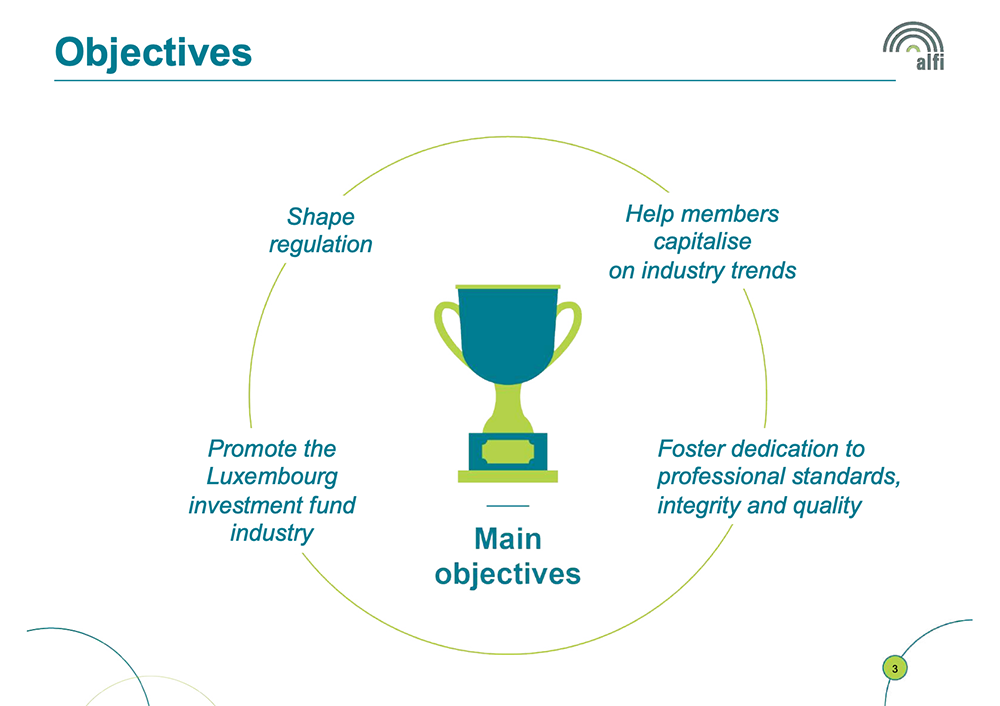

So the objective of the association is fourfold: Together with our members, we shape regulation, and we promote Luxembourg as a core center of competency. We also help our members capitalize on industry trends, and we foster dedication to professional standards integrity and quality. So what does the investment fund industry represent?

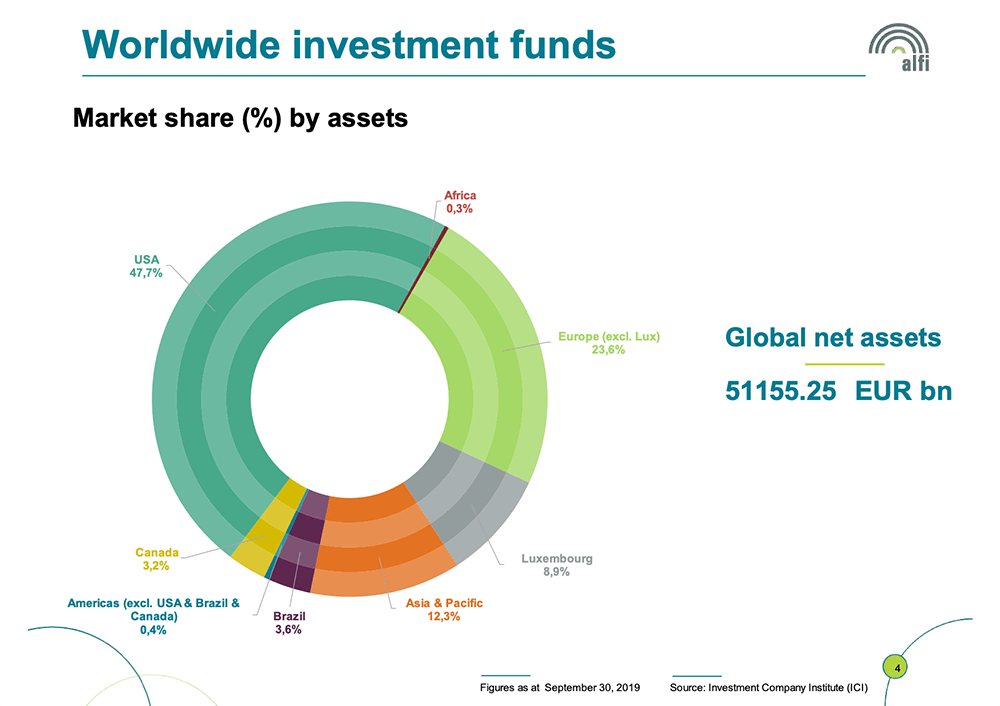

You will very quickly identify that the United States is 47.7% which is by far the biggest player in history, globally. The industry represents €51,255B as of September 2019, and Europe represents a total of 23.6%, and Luxembourg 8.9%.

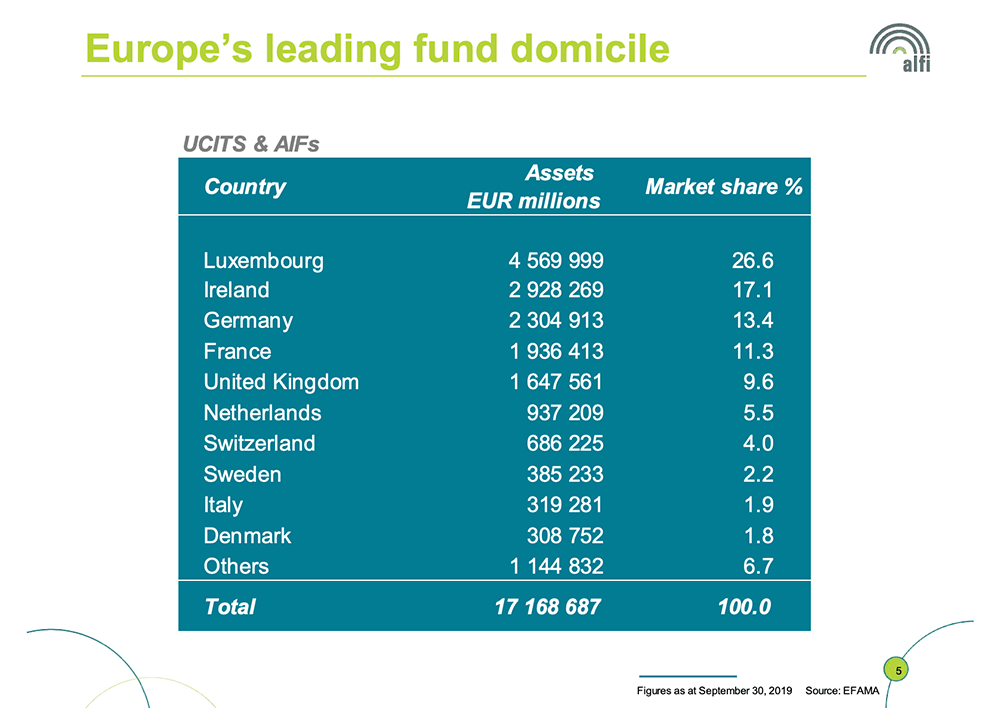

If we go down to Europe, Luxembourg is the absolute leader in terms of assets administration.

Within the Luxembourg Investment Funds industry, we found all types of funds: equity funds, bond funds, balanced funds, money market funds and cash funds, funds of funds and then all the alternative spectrum such as Real Estate funds, venture capital funds, private equity, hedge funds… The Luxembourg fund industry has a very comprehensive ecosystem and it works thanks to this ecosystem. You probably know that all these funds are regulated meaning that they are all supervised by the CSSF.

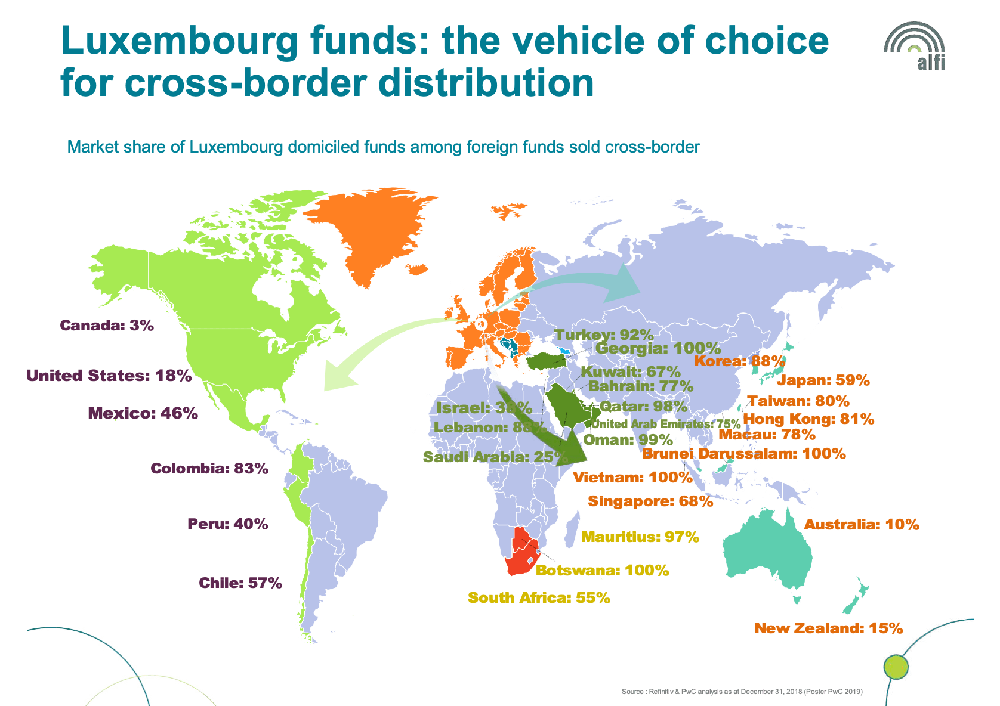

80% of the top 30 asset managers use Luxembourg investment funds as a primary European platform for distribution. So if you have a look on this slide, you see all the big names: Alliance BlackRock, HSBC, Nomura, IMG, Schroders, UBS, and so on. They all have their Funds in Luxembourg. And they all of course administrate and handle the custody here in Luxembourg. Robert already alluded to the cross border distribution of systems.

Of course, those funds are not exclusively distributed to the 550 or 600,000 inhabitants in Luxembourg. But these funds are widely cross-border distributed. If I take for example Hong Kong you see that 81% of all foreign distributed funds in Hong Kong are Luxembourg investment funds. So, this is again proof of the attractiveness of the product.

If you have a look at the world map, we are distributing not only in the Asia region, but across the globe. What are these types of structures and funds that we are best distributing?

We started more or less 40 years ago with UCITS (Undertakings for the Collective Investment in Transferable Securities) funds here in Luxembourg. Then in 2007 came what we call the Alternative Investment Funds Management directive, and that was a third type of practice that we intend to best sell, setting up sustainable responsible investing funds in Luxembourg.

Before I close my presentation, a brief word of digital Fintech Of course in an association like ours, that represents such a huge industry, we are also influenced by digital feedback and developments.

Not late as early 2016, ALFI decided to create what I call the Digital and Fintech Forum. And the objective of this Digital and Fintech Forum is first of all, to follow all the disruptive impacts that digital Fintech may have on the asset management industry, and also identify in the value chains the processes that we could imagine digitalized.

Our primary objective is to build and spread digital and Fintech know-how within our industry by writing white papers, by sharing digitalization initiatives and case studies to be addressed with industry pain points, with FinTech solutions. We regularly cover all sorts of FinTech topics from our conferences and roadshows abroad. And secondary the objective is to create a strong and innovative ICT ecosystem in Luxembourg, and of course, positioning Luxembourg as an innovative asset management center.

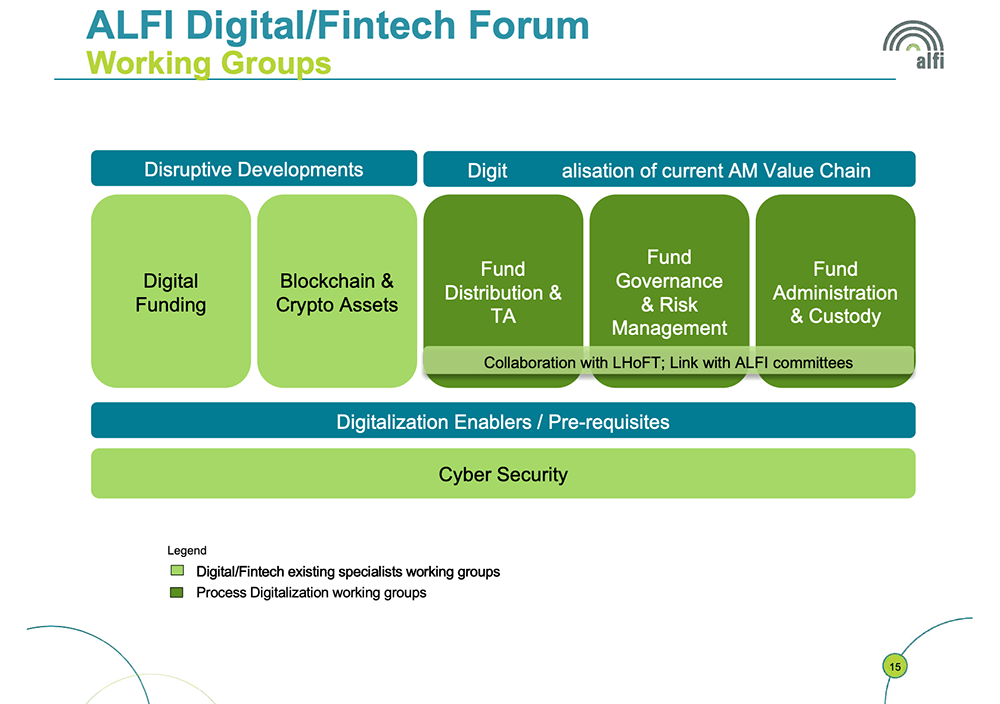

My last slide shows you how the FinTech forum nowadays is being managed. So we have on the lighter green boxes, the digital funding, blockchain, crypto assets, cybersecurity working groups, which are more concentrating on doing deep analyses, writing white papers on answering to a specific consultation set of issues e.g. ESMA.

To give you as an example, with the cybersecurity working group we recently started back in October last year, in a couple of weeks we intend to come out with what I call the best market practice for cybersecurity, what the audience needs to know and to be aware of in the context of cybersecurity, So don’t hesitate to reach out to the ALFI website in the next couple of weeks: you will see some documents that we will publish on that matter.

Recently, we have created additional working groups such as “Fund Distribution and TA”, “Fund Governance and Risk Management”, “Fund Administration and Custody”. These are all process digitalization working groups meaning in these working groups, we try to identify what are the initiatives in the industry, with startups that might impact the activity in these areas. We have more than 120 active members and non-members, non-members being Fintech startups that are active with us in those working groups. We regularly meet, of course nowadays not physically, but digitally. And as I’ve said, we are very active respectively, on each of our roadshows and conferences. We try also to elaborate on digital Fintech topics respectively, together with also our partner associations abroad, we try to bring their local digital Fintech organizations and agendas together so we develop our subjects and topics together. That is that from my part.

Alex Panican, LHoFT

Thank you so much François. ALFI has been very active in the FinTech sphere in Luxembourg. You are always welcoming Fintechs for your amazing conferences and try to connect them with the financial industry. My question to you before I start the presentation about the LHoFT, is there any business to do in Luxembourg for Fintechs?

François Drazdik, ALFI

Definitely, Alex. I’ve been recently contacted by startups from abroad. I recently had a startup from China, on zoom, who contacted me. These people are very active in the governance of investment funds, local investment funds, and they want to come and have a look at what we are doing here. But what I always can recommend to these companies is that they definitely should not hesitate to contact us respectively. They should come to Luxembourg to visit us. And together, we should elaborate on the topics, respectively that he would like to develop. I invited this company to come to one of our next roadshows where we will be present in Asia, beginning of next year, if, of course, the COVID-19 pandemic is under control. Together we will see if that would make sense for him to come physically to Luxembourg and eventually to create a structure in Luxembourg, or become a member of the LHoFT.

Robert Jarvis, LFF

Luxembourg, of course, is a great place to live, and for Fintechs is also a great place to do business as it’s a B2B place for Fintechs. B2C, of course, it’s possible for people to do that, but it’s a B2B place first. I think the best way to explain it is that this fund industry is a huge complex international value chain. So that means if you’re a Fintech doing it, doing AML, doing KYC, doing compliance or anything similar, Luxembourg offers you a platform. And the best example is a Fintech, which I’m not going to mention, but it’s set up in Luxembourg, and their first client after they managed to release a product was a huge global American bank. So of course, it was difficult to onboard but that immediately catapulted them up onto another added value. And then their second client was a huge Swiss bank. Six months later, they’re in the top 50 Fintechs in the world, because if you manage to get those big state streets, or UBS or something like that onto your client base, that’s what Luxembourg can offer. It’s a small country with a huge client base for Fintechs.

Alex Panican, LHoFT

Thank you, Robert, Thank you Francois for all your insights.

I’m going to talk very briefly about the LHoFT. The LHoFT is the Luxembourg House of financial technologies. We are a foundation non-profit, and we are kind of a hybrid. We are a public-private partnership between the Ministry of Finance, Ministry of Economy, the Chamber of Commerce, Luxembourg for Finance, who initiated the LHoFT to start with, plus more than 20 private partners, meaning the banks, the asset managers, and the law firms, as you can see, and the big audit companies we have here in Luxembourg.

Our main mission, together with the fintechs we have in Luxembourg, is to foster innovation in the financial industry.

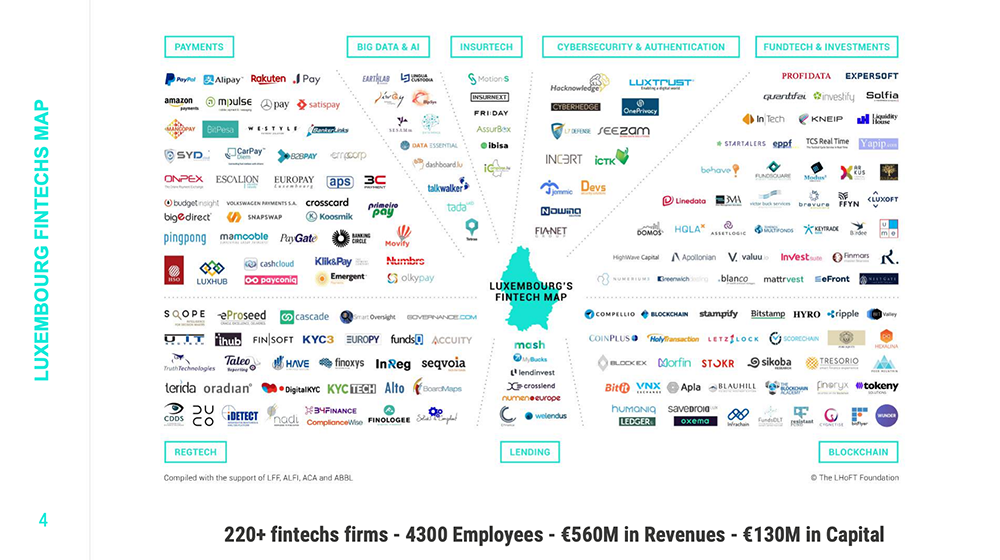

We have more than 220 Fintechs in Luxembourg, they employ more than 4000 employees and they generate a revenue of more than half a billion. And they raised quite some capital last year with more than a hundred million. As you can see, this map is representing Luxembourg. We have the payments side, as Robert mentioned earlier, but we have a huge funtech, regtech, and blockchain ecosystem and all those businesses, most of them at least they are b2b businesses providing services to the financial industry in Luxembourg. And most of them choose Luxembourg for the European headquarter, because most of them are coming from outside Luxembourg.

So why are those Fintechs choosing Luxembourg? We have a huge financial industry. First of all, that’s where they kind of find the clients, but also the legal aspect. Robert also mentioned this passporting license, we’re going to discuss that maybe in the Q&A. The highly qualified people, and also the infrastructure they find here in Luxembourg that so as you can see most of the big players in the world when they choose Europe, usually they choose Luxembourg as the hub to serve. What you will find in Luxembourg is unique. It’s a full ecosystem, a value chain that provides you support from public initiatives such as the LHoFT. There are more than 15 incubators in Luxembourg, not just focusing on Fintech. You’ve got private initiatives, private incubators, and then we have a huge chunk of help regarding financing. That can be some VCs but we also have the European Investment Fund here in Luxembourg, and there is the Luxembourg Future Fund.

Today we host 74 companies. We also have non-hosted members. They are based from Tokyo to San Francisco, more than 150 Fintechs from all over the world while using the LHoFT as a connector to the financial industry in Luxembourg but also in Europe. And so far, for the last three years, we have supported almost 800 Fintechs connected with the local industry. And most of our ecosystem is, as I mentioned, Payments, Regtech, Fundtech, and Blockchain.

We have 14 lockable offices, providing the required security for regulated companies. We provide fixed desks so you can have your address here at the LHoFT and we also offer hot desking. So you come and go as you wish. It’s a beautiful place. Due to COVID, we were a bit more empty, but it’s normally a fun place to be. We are a community. As I said, that’s where people come together to have fun but also to do business.

We also connect you with the universities, having worked with more than 15 universities in Europe. And if you have kids, we also have special programs for kids so they will take care of them. We connect you with the whole world. We work today with more than 20 hubs, again, from Tokyo to San Francisco. If you’re looking to Europe, we connect you with 15 hubs in Europe. So if one day you want to do business in Spain, in France, in Italy, in Denmark, we connect you with the right people over there. So you can also develop your business. So that’s it for me.

Nicolas Gérard, State Street Bank Luxembourg

Thank you, Alex. I’m Nicolas Gérard, and I work for State Street in Luxembourg.

State Street is one of the leading asset servicers in the world. We provide custody, fund administration, and transfer agency for a broad portfolio of clients. Typically institutional clients and investment funds if you want. In Luxembourg, we are very well positioned as a leading custodian and fund administrator.

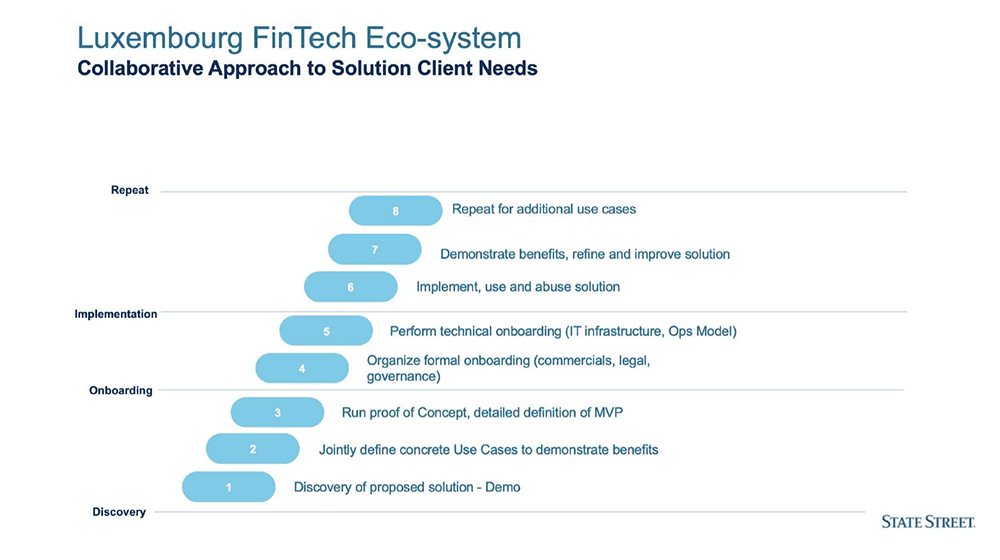

I wanted to talk about a few use cases of how we interact with Fintechs, and the different steps basically of our collaboration with a Fintech. My main message here is that you do not have to sign a contract to provide each other with benefits.

So we have the discovery phase. A Fintech will usually come and give us a demo of the tool, and we will decide if there is interest, if there are common use cases we can work on. We will typically run a proof of concept, and detail a minimum viable product on which we can start. After that if we have a common interest, we’ll work on onboarding the service. That means there’s a set of formalities, which is discussing financials, legal terms, the governance. Luxembourg, as you can imagine, is quite strict on governance. And then that’s where we will implement the solution, I like to say that we will implement, use, and abuse the solution. So that will be good testing and learning grounds for you, okay to know what are further improvements you can do, we will have to demonstrate benefit to our senior management as well. And hopefully, we’ll repeat for additional use cases. So we can always start small, but have an iterative approach. So, the key message is it doesn’t have to go all the way through the eight steps basically to be valuable for each other.

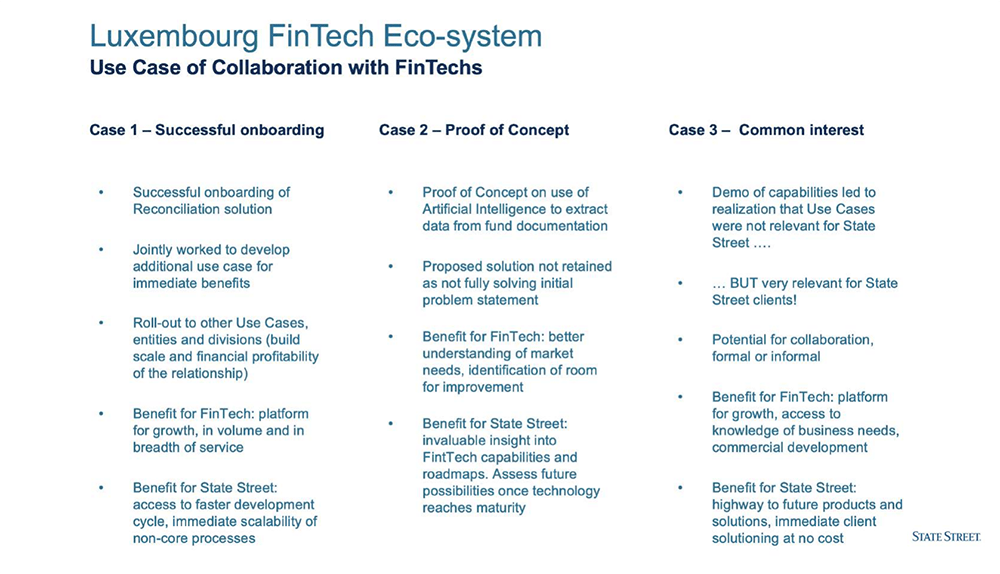

I’ll describe three use cases which are based on real-life, but it’s a good description of what can happen. The first one is a successful onboarding, and I’ve got two cases in mind that were very positive for us. One is a reconciliation solution, the other one is the production and the distribution of UCITS KIDs and PRIIPS KIDs, done with Seqvoia.

By having this level of collaboration, which in Luxembourg is extremely easy due to the size of the country, due to the multicultural aspect of the country, and due to the presence of facilitators like the LHoFT, we can create the links between Fintechs and banks. So due to this collaboration, we manage to quickly arrive at a solution that is scalable on both sides of the equation. In the case of the reconciliation solution, we onboarded one use case for Luxembourg. Very quickly, we also saw that our other affiliated companies in Europe had similar needs so there was a rapid expansion of the collaboration. Very similar to Sequoia. We are always looking at ways to improve the service and ways to expand and go beyond the actual level of service beyond the templates that are provided.

A second use case that I want to present is when we do not manage to reach a contract. So, the use case I have in mind is the usage of artificial intelligence to extract data from documentation. We did a pretty detailed proof of concept, and we reached a common agreement that the solution was not yet there for us. This direct benefit for the Fintech is a better understanding of the market needs. It’s invaluable insight into the technologies which are maybe not sufficiently mature to onboard on a given problem statement, but we at least know the direction of travel and we can assess future product possibilities or process possibilities we can have using a given FinTech.

Finally there are use cases of fintech where very quickly we realized our needs do not meet. So there’s no room to onboard that Fintech, but the solution may be very relevant for our clients. And that’s where there is room for collaboration, whether in direct interest, direct collaboration, or very informal collaboration, to introduce people to each other. The benefit for State Street is again, not direct, but it’s also what I call the highway to future products and solutions. We get to be part of those discussions around the needs, the problem statements, and the direction of travel of the industry.

So really a very, very dynamic, and very collaborative environment in Luxembourg. Usually huge thanks to the LHoFT for facilitating that. So Alex back over to you or Antony.

Alex Panican, LHoFT

Nicolas, if I want to work with State Street, what’s the level of maturity you are looking for regarding the Fintechs or the project?

Nicolas Gérard, State Street Bank Luxembourg

State Street is a bank, a custodian bank. It’s a deposit depository, we are in charge of our client’s assets, we are responsible for the assets, but we are also responsible for the data. So, the first question or the first requirement is to have very solid data protection, process, or procedure. It’s very quickly going to be a showstopper if we cannot demonstrate that our clients data and our data is secure with our Fintech partner. The second thing is to try and that’s very obvious in commercial, you know, commercial science or in marketing, but focus on the problem statement, the problem statement from our perspective as an asset servicer, not the asset manager. So if as much as possible, a FinTech, that comes with a business case, with a use case, very well described, and very easy to understand, this business case will help us also sell the solution to all stakeholders internally. Empathy and security.

Alex Panican, Head of Partnerships and Ecosystem, LHoFT Foundation

In the selection of the Fintechs to work with, are you giving priority to the ones based in Luxembourg? Or are you just based on quality?

Nicolas Gérard, State Street Bank Luxembourg

No, there’s no priority to Luxembourg. Quality first.

Robert Jarvis, LFF

What we really care about is that our financial center remains competitive. And if we have a Fintech, I can sell their products to financial institutions in Luxembourg, thereby making them more efficient. That’s great for Luxembourg. That’s great for the industry, no matter where you’re based, as long as it’s allowed. So maybe you need to be regulated. Maybe you don’t. But as long as it’s legal and compliant, no matter where you are, that’s fine for the industry in general. And if you do need a place in Luxembourg, the LHoFT is usually the best place to get started.

Alex Panican, LHoFT

Thank you. Very nice. Francois, do you want to add something? Are you giving priority when companies are contacting you? What is the selection process?

François Drazdik, ALFI

As Robert said, it’s more about the attractiveness of the solutions and effects of startup would like to develop your maximum.

The other point that I wanted to make is, as I said, we are regularly traveling around the globe. So we are going to what we call our famous roadshows in all areas of the world and in these various cities that we show up. So we regularly have nowadays also questions on digital Fintech developments here in Luxembourg, and interest is huge. So there are a lot of contenders in the world who heard about the developments here.

The last point that I wanted to make is about foreign startups who contact us at ALFI, saying: “Hey, listen, guys, I want to come to Luxembourg.” And what I recommend to these people is if next time so you are around and we have one of our large conferences, for example, Luxembourg, I offer them a ticket for free I invite him to come to participate in that event. I invite people to come along and spend a few days with us, distribute business cards, listen to our topics, exchange ideas, and it is through that means that such people get confident in eventually thinking about okay should I go now a step further with settling down in Luxembourg. Perhaps starting with a place at the LHoFT to get a foot into the door.

As our major conference will not take place this year, we are working on the digital events video conference. It’s an event that will be organized all over the week of the 15th of September. So meaning we’ve come up with a number of plenary sessions, and with a number of other topics that you would like to develop, where to outgrow some of the format of panels, or we go ahead and we record sessions, some of them and we put them at the disposal of the audience, first of all, to follow life respectively, in a second stage to retrieve from YouTube or from Twitter or LinkedIn wherever we publish that.

Alex Panican, LHoFT

Perfect, thank you so much. We’ll keep people updated on that. Quick question. You mentioned about setting up the business. So I’m going to just ask Hugo, who is working for Finnimo, one of our accounting partners. Do you know how much it costs to set up a business in Luxembourg, and how long it takes?

Hugo Vautier, Director Fund Administration at Finimmo Luxembourg SA

This is a very complicated question. Thanks for asking that. It really depends on the type of business and the type of company. So basically, if it’s a simple commercial company, it’s quite straightforward. So it’s a matter of weeks to get the company up and running. And the cost is roughly, let’s say between five and 10K euros depending on the legal advisor you may use and it also includes the notary fee for the incorporation, etc. I would like to draw your attention to the fact that the main bottleneck of this process is the bank opening process, the bank account opening process. So as long as the bank account is open, the incorporation itself is a matter of days.

Alex Panican, LHoFT

As we work with many banks, yes, we can also facilitate that. Before giving the mic to Susanne in one second, if you don’t mind. A question to you because you mentioned what kind of legal entity and that’s a question more for Nicolas and François We have some companies asking us if they need to be PSF to serve the financial sector and to work with the asset management in Luxembourg. What’s your intent guys on that? So just explain PSF what it is and so, what’s up?

Robert Jarvis, LFF

In Luxembourg, many Fintechs have to be regulated to a certain extent. And there’s something we’d like to call PSF. It basically means “professional in the financial sector”. And I have kind of like an idiot test, it’s basically, do you touch confidential data? Yes or no. And if you do, most likely, you will have some kind of regulation, meaning that you understand how to handle the data means that data is stored safely, etc. But, you know, because of the number of financial institutions in Luxembourg, even I would say a cleaning lady or an organization provides cleaning services, you know, they move around the office, they see confidential data, even those need to be regulated as a type of professional of the financial sector. So, so many Fintechs do, unless you’re a pure software provider that doesn’t actually see the data, but it’s nothing to be scared of. And in fact, the PSF kind of is a label of quality, it means that you have your Risk Management and your compliance and then your operations have been under control. That’s how we’d like to see it in Luxembourg.

François Drazdik, ALFI

I think particularly in the investment fund industry, it’s always a question of credibility. Meaning if you come to an industry like that, which is extremely well regulated in Luxembourg, it also makes sense, whatever type of activities that you offer, that would be regulated.

Nicolas Gérard, State Street Bank Luxembourg

It really depends on the type of activity, which the Fintech will support us on if the activity is regulated. And if the data is accessible, accessible to the, to the Fintech, then it is preferable to have the PSF status. But otherwise, it’s not required. It’s always easier because it facilitates basically our governance and the level of oversight and due diligence we have to perform on the Fintech. But it is not a must have, again, depending on the type of activity and regulation.

Alex Panican, LHoFT

I’m just going to give the mic to Susanne because Susanne is working with Seqvoia, already mentioned by Nicolas, and maybe she can give us feedback how it is to be a Fintech in Luxembourg and work with the fund industry.

Susanne Schartz, COO of SEQVOIA

I was just offering a bit of a testimony from the other side. Seqvoia is a Fintech even though we’re not the smallest Fintech anymore. And we’re already working with some large financial institutions in Luxembourg and Europe wide. But really, what I see as the big advantage of Luxembourg is that proximity, so we’re a member of ALFI as well. I’m participating in some of the working groups that Francois has mentioned, we are a member of the LHoFT, where we are speaking to clients and to other members of the finance community to understand the market see what’s happening, see the direction that certain things are going be it regulation, the legal situation, the client needs… And this is extremely useful, especially because there’s a big spirit of collaboration in Luxembourg so that it is much easier than in other places to get feedback to present an idea to somebody from the industry and then get honest feedback saying, well, that’s good. That’s not good. It’s, you know, it’s beside the point. It’s beside the point for us, but maybe another client type would like this. And I think that’s quite unique in Luxembourg.

Alex Panican, LHoFT

Susanne, if you gave advice to entrepreneurs coming to Luxembourg and working with the financial industry, what would it be?

Susanne Schartz, COO of SEQVOIA

I would tell them to have very, very open ears. Be humble, rather than you know, come and do the big sales presentation. Yes, it might be sales, but be there to actually make an exchange. And for this, you have to be open to hear what the other side says, especially if it’s something that you don’t really want to hear. So that is important. And then you know, then offer your services or work on something, what can we do to show what we’re doing to understand. That would be probably my first advice.

Robert Jarvis, LFF

I am jumping on the collaboration aspect. But the advice I would give to a Fintech: If you want to do business in Luxembourg, get connected to the LHoFT. You don’t need to live at the LHoFT. You don’t need to be regular there. But the LHoFT has created a community in Luxembourg, which is second to none, and like Susanne was saying, a community that works together. And I think that’s because of the fact of how our financial center is. It’s International. Remember that map I showed at the beginning? You know, people would like to pretend to work together because their clients are actually somewhere else, you know. Nicolas’ clients from State Street might be in the US. But that doesn’t mean that Nomura bank which has clients in Japan doesn’t have some of the same problems. So often, people find in Luxembourg that they have the same problem internationally, and the LHoFT helps them connect with their solutions. That’s the one big game-changer that’s happened in the past four years is that the LHoFT has really brought the industry together and pushed it into a similar direction.

Nicolas Gérard, State Street Bank Luxembourg

Very difficult question. The biggest advice: it’s really along the same line, be connected. Make sure you get to grips with the regulation, and that an activity being more regulated than others doesn’t make it less appealing. They may be more challenging, but that also drives the need for solutions.

François Drazdik, ALFI

Our mission, of course, is to continue growing, continue attracting new funds and new structures, complex products. In Luxembourg, it’s not always exclusively about regulation and new regulations that will allow us to grow but it’s also about efficiency. And efficiency now goes hand in hand with new developments, new out of the box ideas, and these ideas definitely come from startups and therefore so it’s a place to be.

Alex Panican, LHoFT

Thank you guys so much for sharing your expertise, your experience.