At the LHoFT, we strongly believe that financial technology is crucial to advancing financial inclusion, empowering groups that have been left behind by the traditional financial system. Whether it’s financing for entrepreneurs, pension products for the underbanked, specialised insurance plans or even financial education and literacy aids, the positive impact being driven by entrepreneurship is improving lives around the world.

Building on the success of the first edition of the program in 2018, CATAPULT: Inclusion Africa 2020 is a unique one week program of Fintech startup development built by the LHoFT Foundation, targeting African Fintech companies, focusing on creating bridges between Africa and Europe and aligned with the sustainability goals of Luxembourg’s finance centre.

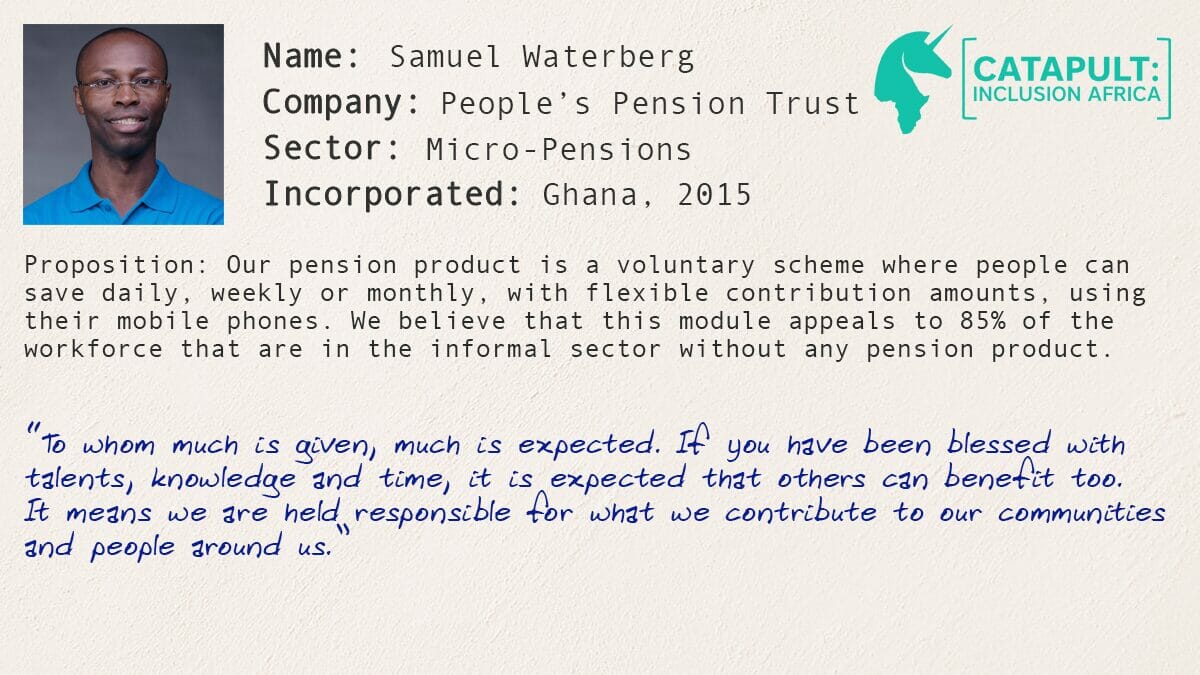

In the run up to our Financial Inclusion bootcamp, we will be sharing insight from the founders participating in this year’s edition, continuing with Samuel Bediako Waterberg, CEO of People’s Pension Trust:

“Financial Inclusion is about people, not numbers. Does your product or service elevate people from (real) poverty or are you focused on the number of people signed up for a product or service?” – Samuel Bediako Waterberg

Can you tell us a little about yourself and your company?

I’m a Ghanaian who lived in the Netherlands for 22 years. I have a master’s degree in Strategic Management from the University of Tilburg, and a banker by profession. Before returning to Ghana in 2011, I worked for the Rabobank in the Netherlands for 7 years..

Currently, I am the CEO of People’s Pension Trust Ghana Limited, an innovative award-winning pension fund. A pension company dedicated for the workers in the informal sector. People’s Pension Trust provides pension product for farmers, market women, small scale enterprises, the self-employed and those working in the informal economy. Clients can save daily, weekly or monthly, with flexible contribution amounts, using their mobile phone (mobile money) or via cash payment.

What were you involved in before People’s Pension Trust which led to the development of this idea?

After returning to Ghana in 2011, I started a hospital. While in Ghana, I realized that my uncles and aunties, who were self-employed (entrepreneurs) in the informal sector and now on pension were dependent on their children to cater for them in their old age. Looking back, when I was a young boy living in Ghana, these same uncles and aunties will bestow gifts on us during our visits and were financially sufficient. Fast forward to today, the tables have turned. They are likely to end up in old age poverty or be dependent on their children now that they are on retirement because they didn’t have the opportunity to save for their retirement as informal sector workers.

Experiencing this contrast within my own family was an eye opener. It brought me face to face with the sad reality of the majority of working Ghanaians. Without any form of pension or social security, we become reliant on our children and community, often burdening them with a responsibility we would rather carry ourselves. This was my motivation for starting People’s Pension Trust and founding a company that prides itself in developing innovative yet simple ways of getting traders and other informal sector workers such as my uncles and aunties to prepare adequately for retirement.

How big a part do pension products play in the overall picture of financial inclusion and fighting poverty?

Looking at financial inclusion, people tend to look at individuals and businesses having access to useful and affordable financial products and services that meet their needs. Most often, people have a tendency to look at the present need like having a bank account, savings account, payments, credit and insurance. People have a propensity to forget the long term needs, when the same individuals go on retirement. With life expectancy increasing, the cost of living going up and the breakdown of joint family structure in sub-Saharan Africa, people are ending up in old age poverty when they go on retirement. The government doesn’t provide social pension, meaning that people will be dependent on their family or end in old age poverty for 10 to 15 years of their retirement life. It’s expected that by 2050, more than 500 million people in developing countries will be over 60 years. Currently 480 million in Africa are in the informal sector, which is 85% of the workforce without any form of pension.

What advice would you offer to other founders looking to increase Financial Inclusion in Africa?

In providing Financial Inclusion in Africa, don’t only focus on the immediate need of the people, but also the long-term needs. There is no point in providing Financial Inclusion which helps people in the short term, and brings them back into poverty in the long term.

Financial Inclusion is about people, not numbers. Does your product or service elevate people from (real) poverty or are you focused on the number of people signed up for a product or service?

Is your product or service sustainable in the lives of the people? Does it make business sense? Financial Inclusion projects that are driven by project funding end when the funding is depleted.

Use technologies that are understandable, affordable and benefits the people you are serving. If the right technology is used, there is the potential to extend financial inclusion to the world’s poor..

What are you hoping to get out of your experience at CATAPULT: Inclusion Africa?

I am expecting to meet like-minded entrepreneurs with similar goals to exchange best practice knowledge, learn from peers and stay abreast with the latest industry developments. I also look forward to building a network of entrepreneurs across the continent, developing long-lasting business relationships, getting fresh ideas to help me grow my business and sharing my experiences with fellow entrepreneurs. Lastly, I hope to meet potential investors to scale up the business.

What’s next for People’s Pension Trust? What do you see as the key challenges as you grow further?

People’s Pension Trust wants to grow the customer base to 500,000 people by 2024, unlock long term savings of EUR 60 million in assets under management in Ghana and scale the business to other sub-Saharan African countries.

The key challenges are to transcend from High Touch to High Tech, where 90% of all contributions will be received digitally (via mobile money or bank account) and maintaining trust amongst your customers and potential customers with all the negative things that happens within the financial sector.

Lastly, scaling up in terms of funding and finding the right partners for the scaling up.

What does ’financial inclusion’ mean to you?

Financial Inclusion is helping people to improve their quality of life and helping them to be more resilient for life shocks that might take place. This is possible by providing financial products and services that meet the needs of vulnerable and low-income groups at an affordable cost, in a transparent and accessible manner.