In my first contribution to this blog back in May, I discussed barriers to financial inclusion and some of the literature supporting the link between financial inclusion and economic growth. While the link between the growing use of mobile money services and other fintech applications in the developing world and financial inclusion was commonsensical, formal research into the subject was lacking.

Earlier this month, researchers at the IMF made an important contribution to the literature by examining the link between fintech adoption and financial inclusion more closely.

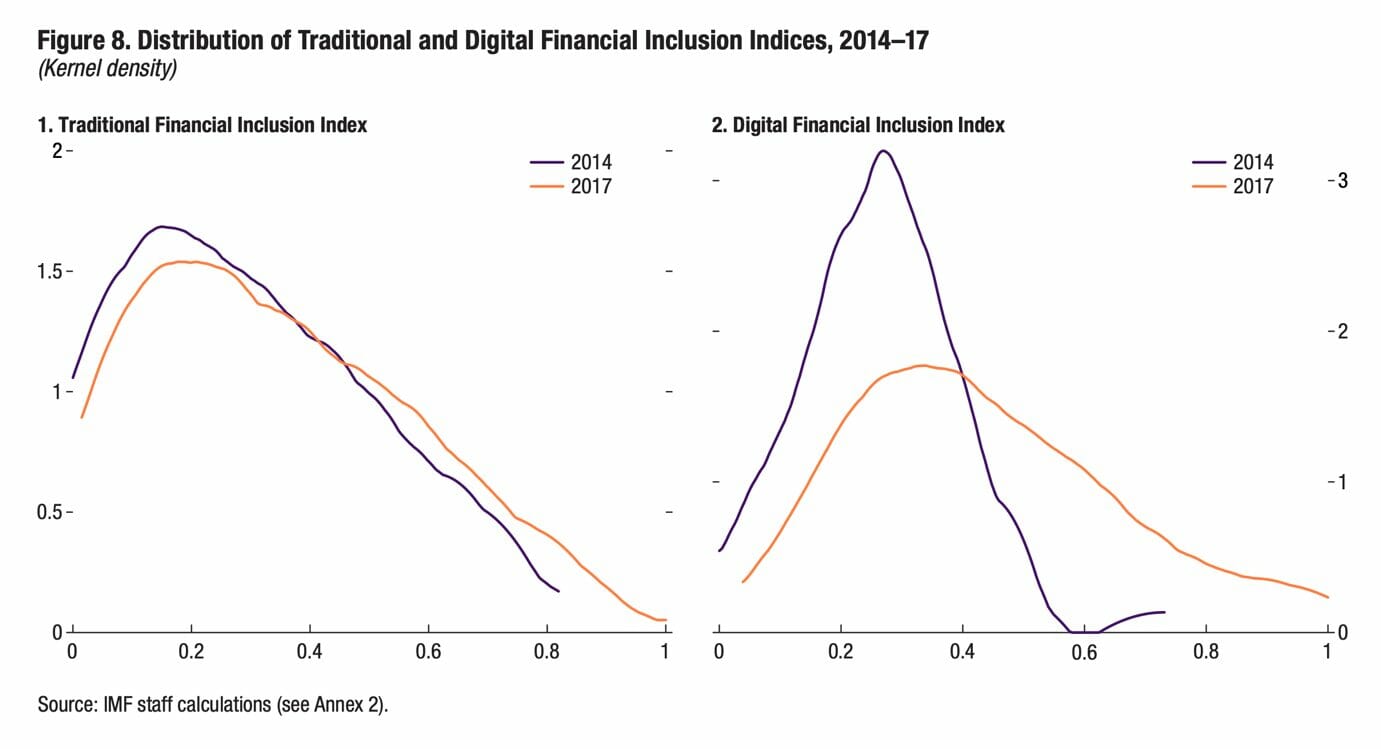

When approaching the topic of financial inclusion and why we should care, I always find it helpful to step back and ponder the sheer scale of the challenge: “globally 1.7 billion people have no access to a bank account and small- and medium-sized enterprises (SMEs) (95 percent of companies worldwide) provide employment to more than 60 percent of workers, yet struggle to access finance”. As the above graph from the IMF paper convincingly shows, digital finance / fintech contributed more substantially to driving financial inclusion between 2014 and 2017 than traditional finance. Some of this is a matter of means – mobile phones have become widely available even in the poorest geographies, facilitating the spread of mobile money services – but mindset also matters. Traditional financial institutions with a presence in relevant geographies but without investment in mobile money and other technologically enabled services that drive financial inclusion need to ask themselves just why they continue to miss out on one of the most pronounced, and socially impactful, opportunities in all of finance. Consider the following: “The number of active mobile money accounts almost tripled and the use of mobile phones for domestic remittances roughly doubled between 2013 and 2017 in lower-middle and low-income countries. As a result, in low-income countries, about half of the population received or sent remittances using mobile phones in 2017. The value of mobile money transactions now constitutes a substantial part of the financial system, with transactions in Cambodia, Ghana, and Zimbabwe, reaching more than 75 percent of GDP in 2018.”

These trends are no longer confined to the developing world:

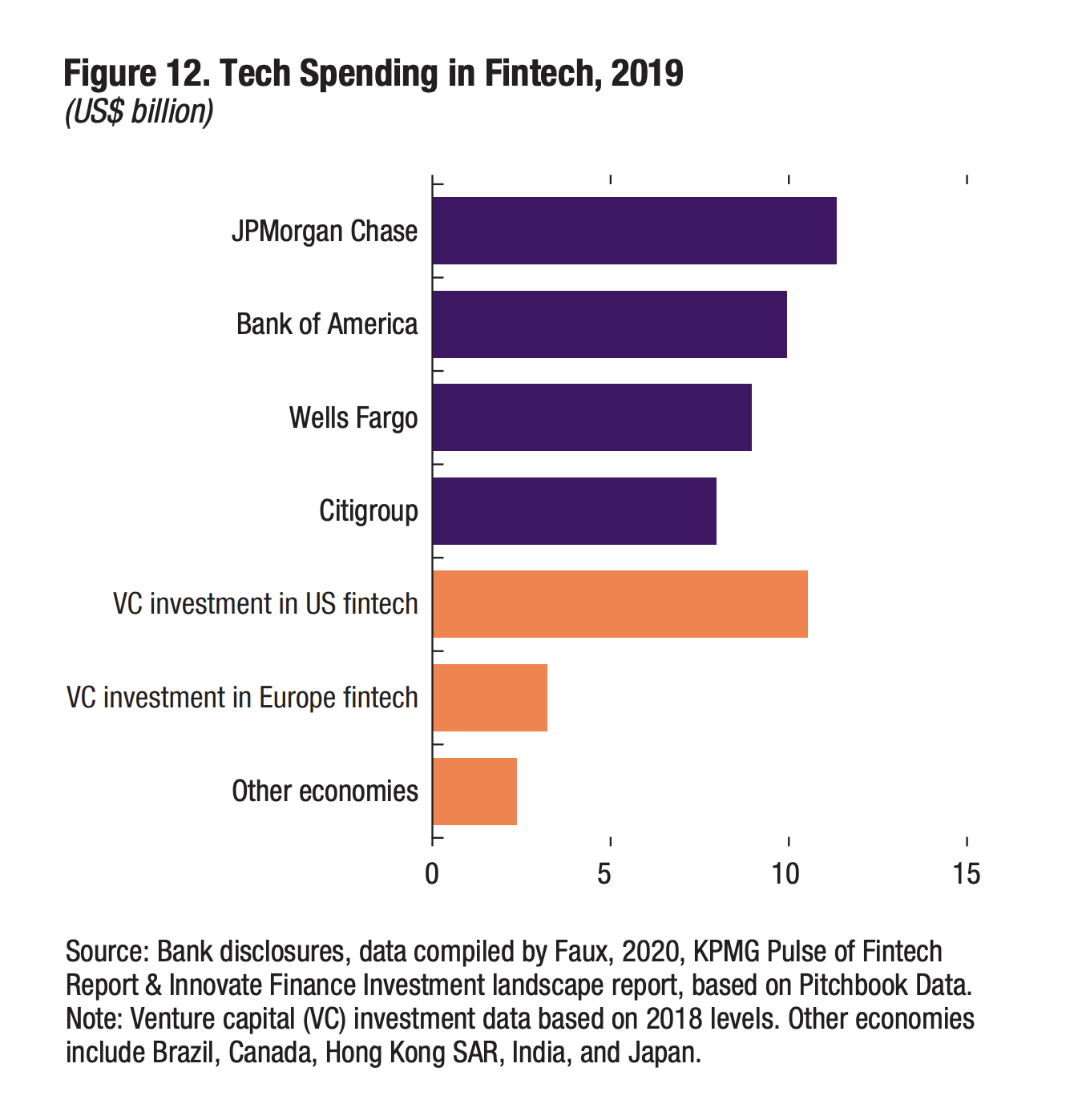

“Fintech companies in the United States have grown to make up 38 percent of the unsecured personal loan market in 2018, from only 5 percent in 2013 (TransUnion 2019). In the United Kingdom, SMEs are an obvious target of fintech companies as they receive only 2 percent of bank loans, even though they contribute to 50 percent of GDP and 70 percent of employment.”

The need for services which complement traditional bank offerings is real; a wealth of data and algorithmic prowess (AI) is ready to be leveraged, and if you won’t invest, your competitors will:

Speaking of investment & publicity; Fintech / Regtech startups active in financial inclusion have until August 15 to apply for the 2020 showcase hosted by the Alliance for Financial Inclusion. The AFI showcase offers a unique opportunity to present in front of “AFI’s membership of central banks, ministries of finance and financial regulators from more than 80 developing and emerging countries”.

ESG continues to go mainstream

An additional consideration for laggards in this space is that financial inclusion is part of the “S” in “ESG”, and that investors continue to place growing emphasis on ESG for their capital allocation decisions.

A few years back, as a member of the reporting and assessment team at the Principles for Responsible Investment, I had a chance to witness firsthand the tidal wave of ESG implementation in the asset management community, as well as the challenges flowing from the evolution in the massive datasets that resulted from the PRI’s reporting exercise. While the debate around ESG data and its interpretation continues, these were, and continue to be, growing pains: in 2017, the PRI’s membership already comprised the majority of global AUM (>$60tn), and this has now exceeded $100tn.

It follows that ESG is not a “fad” and rather a fundamental shift in how investors value and evaluate assets and asset managers.

Beyond the adherence of asset managers to PRI, the fulsome implementation of ESG considerations into standard reporting practice has recently been cemented by accounting standard bodies, regulators and policymakers. For instance, IFRS in November 2019 provided guidance on the implementation of climate-related disclosure, drawing on recent Australian guidance on climate risk materiality to reiterate that “qualitative external factors, such as the industry in which the company operates, and investor expectations may make such risks ‘material’ and warrant disclosures in the financial statements, regardless of their numerical impact.” Circumstances and stakeholder expectations – changes in priorities and mindsets – define what is material and what is not.

Beyond shareholders, citizens at large are of course key stakeholders in seeing ESG implemented into commonplace investment and reporting practice – we all have an interest in seeing an equitable and sustainable society unfold for ourselves and our offspring. In the EU, citizen’s interests in this realm have been served most visibly by the implementation of a EU taxonomy for sustainable investment – an EU-wide classification system that provides businesses and investors with a common language around sustainability. In the context of manifold ESG and sustainability initiatives, associations, labels and standards around the globe, defining this common framework for the EU is a concrete and valuable step towards a more frictionless and more impactful development of the space. Criteria for inclusion in the taxonomy are summarized here.

While the EU taxonomy lays crucial groundwork for a transition towards a more sustainable economy, individual companies still need to contend with how best to advance ESG implementation inside their organization, taking into account their growth objectives and the specifics of the industry they compete in.

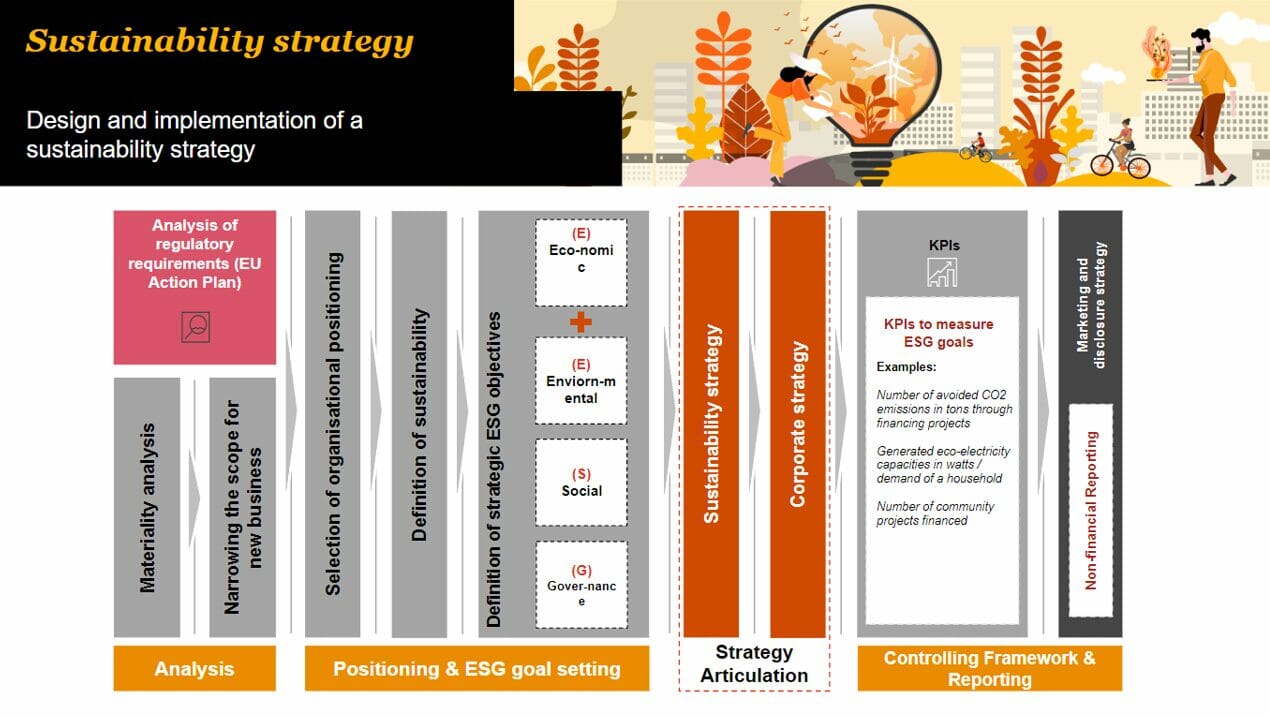

Our partner PWC recently provided guidance on how to design and implement a “sustainability strategy” premised on a sequential approach, flowing from materiality assessment & regulatory compliance into strategic positioning, internal controls and reporting.

With regard to materiality, PWC echoes the IFRS in stating that “It’s imperative that businesses understand what the ESG-related priorities for employees and external stakeholders are. Their concerns and expectations will be the base for the top management to get primary information on the issues to prioritise according to their importance to the company’s mission and stakeholders’ expectations”. Furthermore, businesses need to pay heed to regulatory and policy developments, notably the taxonomy and other aspects of the EU action plan on sustainable finance as these will “impact how investment firms make investment decisions and distribute financial products, and how they incorporate ESG into their business operations and strategy”. Just as the PRI has driven alignment between asset managers and the asset owners they serve, EU policy on sustainable finance and the taxonomy will drive alignment between corporates and the financial markets.

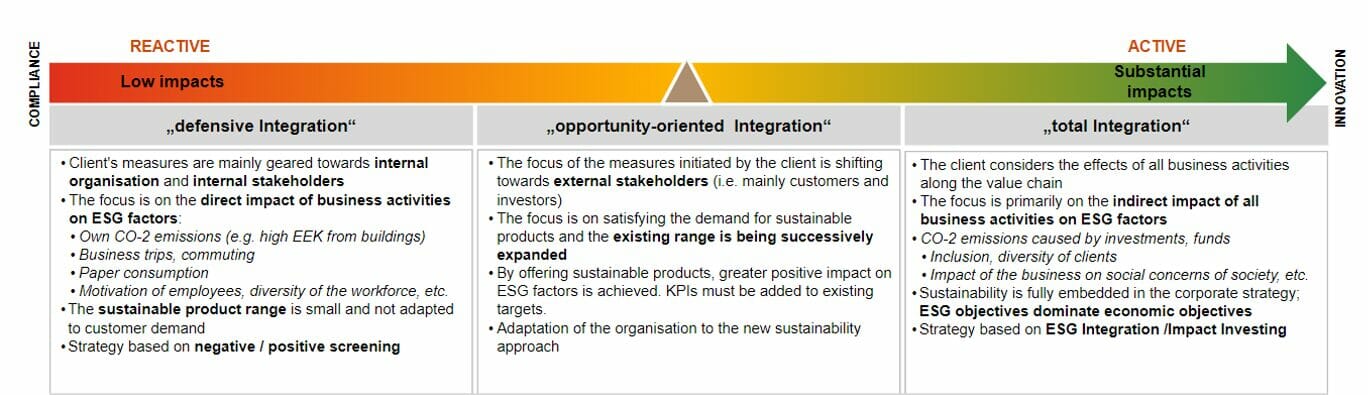

In another parallel to dynamics in the asset management industry, corporates need to decide whether they wish to implement ESG considerations rather more defensively or more proactively. As PWC note, the natural choice for many businesses will be a bare-bones implementation in order to comply with minimum requirements and expectations, but over time as businesses accrue experience with this newfound aspect of their strategy, they should begin to see ESG implementation and reporting as a competitive advantage and hence a strategic opportunity.

We’re all in this together

Nobody operates in a vacuum.

The tremendous strides made with regard to financial inclusion have been very substantially driven by financial technology. Services not offered, and clients not served, by traditional financial institutions, will flow to newcomers. Invest, or miss out.

In an interconnected world, growth and social stability, as well as the lack thereof, in any given part of the world has repercussions elsewhere. Economic interests and ESG considerations have become intertwined and this change in priorities and perceptions will continue to be fortified by the pressing and unrelenting challenges posed by climate change and global development.

COVID-19 has prompted the financial industry to accelerate the implementation of advanced technological solutions with a view on operational resilience, and we were glad to hear directly from key decision makers in the Luxembourg financial centre during our recent CEO roundtable:

Together, the drive towards greater implementation of financial technology, ESG and financial inclusion will continue to shape the world we live in. At LHoFT, we are proud to act as an accelerator of such change, and we continue to support our partners and members in their journey.

Author: Jérôme Verony – LHoFT Research and Strategy Associate