Progress and urgency

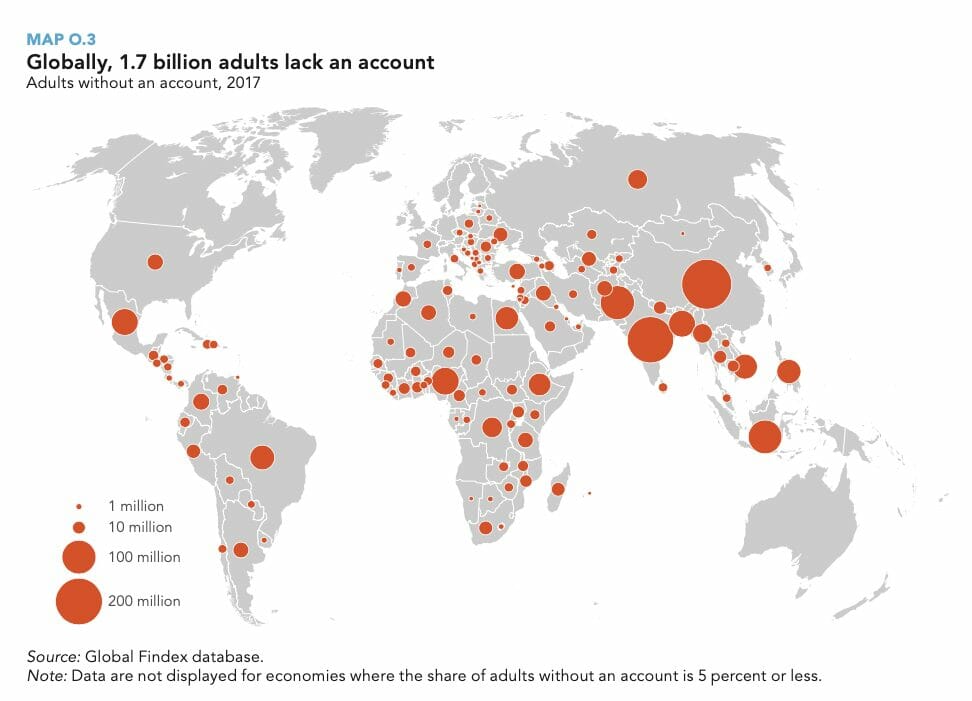

In the 10th year following the creation of the Global Partnership for Financial Inclusion, the financial inclusion movement can look back on significant accomplishments, best captured by the fact that more than 1.2 billion adults have obtained greater access to the global financial system via a bank or mobile money account since the G20 nations formally committed to making financial inclusion a political priority. However, 1.7 billion adults remain unbanked and significant disparities remain – for instance, women remain underbanked relative to men in developing countries.

Image source: Global Findex Database 2017

The unfolding economic shock resulting from the COVID-19 pandemic makes financial inclusion an even more pressing topic than before, as we are likely to see the first increase in global poverty since 1998 and the ripple effects of the crisis are likely to hit the world’s poorest and least connected the hardest. Investing in financial inclusion means investing in improved livelihoods for billions, a more resilient and sustainable financial system and at the end of the day, economic growth. Just as leaders are urged to tie fiscal stimulus to a transition towards a more environmentally sound, sustainable economy, financial inclusion should be pursued with urgency if we are to lessen the negative effects which follow from rising income and wealth inequality. A sustainable economy is not least one that benefits all participants.

Overcoming barriers

Fundamentally, financial inclusion is as much an economic question as it is a social one. Extending access to financial infrastructure and services to all adults equals maximizing the pool of consumers, savers and market participants. The Global Findex Database 2017 report acknowledges the crucial role of financial technology in making global financial goals a reality and cites examples of financial inclusion enabling the rural poor, especially women, to move away from a bare-bones subsistence economy towards a more entrepreneurial and connected existence. Presciently, the report also highlights that financial inclusion serves to lessen the impact of economic shocks such as the one induced by COVID-19:

“Digital financial services can also help people manage financial risk—by making it easier for them to collect money from distant friends and relatives when times are tough. In Kenya researchers found that when hit with an unexpected drop in income, mobile money users did not reduce household spending—while nonusers and users with poor access to the mobile money network reduced their purchases of food and other items by 7–10 percent.”

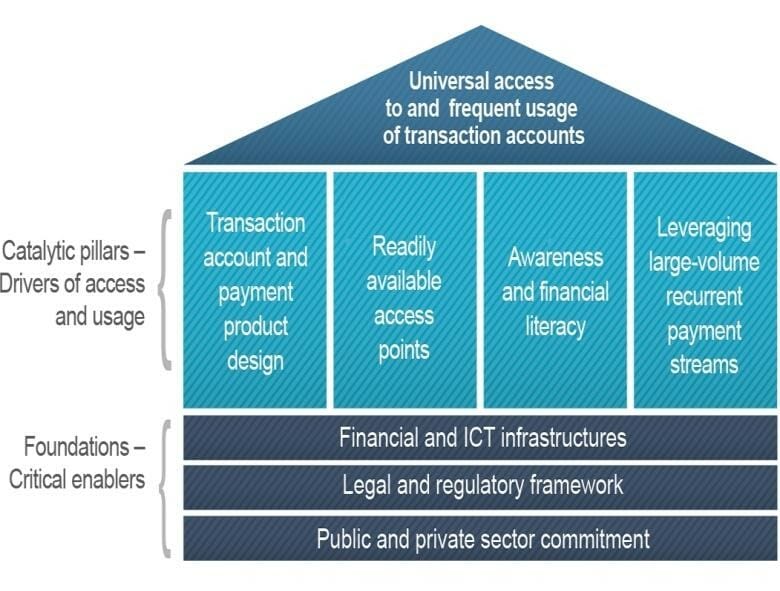

Given the above, what is holding financial inclusion back? Researchers analyzing the barriers to greater financial inclusion have found that account costs are among the most significant and persistent factors negatively impacting financial inclusion. Fintech has a crucial role to play in lowering those costs and thus, removing the most important barrier to financial inclusion.

Image source: The World Bank

Looking at the macro level, research focusing on Asian economies suggests that greater financial inclusion negatively impacts financial efficiency as a result of (initially) high information costs and increasing information asymmetries. The same research finds that financial inclusion positively influences financial sustainability and lists “diversifying bank assets, and thus reducing their riskiness; increasing the stability of their deposit base, reducing liquidity risks; and improving the transmission of monetary policy” as likely contributions to these findings.

What we can learn from the above is that onboarding the unbanked presents with non-negligible challenges but that the effort is more than worth it from a socio-economic perspective. Information asymmetry can and should be reduced via public and private sector efforts to strengthen financial literacy.

Empowerment via technology

That such efforts bear fruit should be evident from recent history.

The rapid development of e-commerce and digital innovation emerging from many Asian economies for instance shows that economies can rapidly transition from a largely subsistence-based model to sophisticated, highly interconnected and productive structures that create enormous amounts of wealth and which have lifted hundreds of millions out of poverty. As the example of China demonstrates, such swift and profound transformation can occur in political and cultural contexts that are vastly different from the Western model. Human progress is fundamentally driven by attributes which we all share regardless of our cultural, ethnic and political differences: a profound motivation to improve upon our livelihoods and to lay the groundwork for an even more prosperous future.

Just as the human drive towards progress is universal, technology is agnostic towards those who wield it, and to the ends they pursue.

It is hard to think of an area in which financial technology has played a more crucial role than in the ongoing drive towards universal financial inclusion and the resulting, positive impact on the livelihood of hundreds of millions of people around the globe. It is not difficult to imagine that those who champion and facilitate financial inclusion today will reap the benefits of their efforts in the years to come.

At LHoFT, we are committed to supporting the sort of innovators who will continue the drive towards universal financial inclusion by removing obstacles via technology-driven solutions. We are proud to share that one of our Catapult: Inclusion Africa participants (uKheshe) was recently selected to participate in the Mastercard Start Path program, and that yet another (Symplifi) is partnering with Shieldpay to expand its platform in Europe.

We are confident that more is to come, and we look forward to advancing on this journey with our industry and public sector partners.

Author: Jérôme Verony – LHoFT Research and Strategy Associate