The rapid evolution of artificial intelligence (AI) and other technologies is revolutionising the banking industry, presenting both new opportunities and significant risks. AI and machine learning (ML) are being used in credit underwriting, fraud detection, and customer service, enhancing efficiency and risk management. However, these technologies bring strategic challenges, such as competition from fintech, operational challenges with legacy systems, and reputational risks from potentially unfair outcomes.

Regulatory bodies, like the Basel Committee on Banking Supervision, are evolving frameworks to ensure responsible innovation. Initiatives such as the EU’s Digital Operational Resilience Act[1] aim to strengthen financial entities’ resilience against ICT-related incidents. To stay competitive banks must balance innovation with risk management, foster collaboration with regulators and technology partners, and adapt to the changing digital landscape.

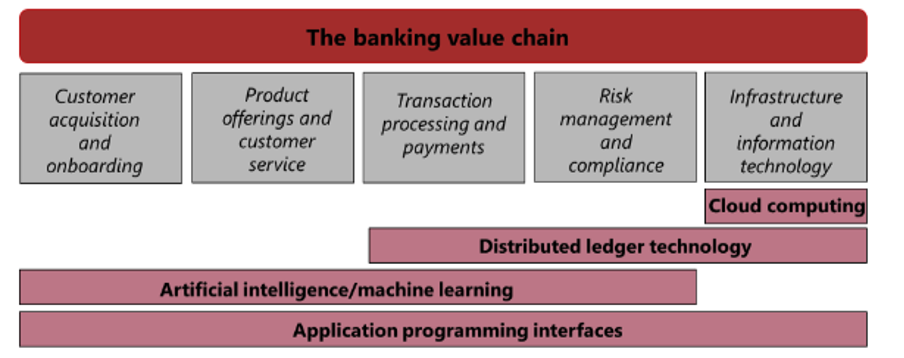

Innovative technologies and applications

The Basel Committee on Banking Supervision recently published a report[2] which considers the implications of the ongoing digitalisation of finance on banks and supervision. The section on “Innovative Technologies and Applications” presents several key technologies driving this phenomenon.

- Application Programming Interfaces (APIs) are pivotal in facilitating data sharing between applications, enabling real-time processing, and enhancing data connectivity. Banks leverage APIs for various functions, including mobile and open banking applications, where the financial data can be shared with third-party providers for personalised products and services; and internal system data management.

- Artificial Intelligence (AI) and Machine Learning (ML) are increasingly employed by banks, particularly in customer-facing services and revenue generation. These technologies allow computers to perform sophisticated tasks that previously required human intervention. The adoption of AI/ML technologies varies among banks, reflecting different levels of interest and implementation.

- Distributed Ledger Technology (DLT) is recognised for its role in providing secure, transparent, and decentralized record-keeping. Though specific details are sparse, DLT is acknowledged as a significant influence on the financial sector[3], shaping how transactions and data are managed.

- Cloud computing is another crucial technology being widely adopted by banks. This trend is set to continue, indicating a growing reliance on cloud services for various operations within the banking industry.

All these technologies play a crucial role in reshaping the banking landscape and are essential components of the digital transformation in the financial sector.

New competitors and business models

The innovative technologies mentioned above have enabled the rise of new digital-only participants in the financial services sector, including neobanks, fintechs, and larger technology companies. These new competitors often hold advantages in data and technology, operating on digitally native platforms without the burden of legacy IT systems. This shift is reshaping the competitive landscape, particularly in payment services.

This influx of new entrants and the adoption of advanced technologies have prompted traditional banks to form strategic partnerships with various firms. For example, J.P. Morgan Payments provides embedded banking services on e-commerce platforms like Amazon, Macy’s Marketplace, and SalonCentric, serving as the invisible provider of banking services[4]. Goldman Sachs partnered with Apple to launch the Apple Card, a credit card integrated with Apple’s ecosystem[5]. These collaborations are transforming traditional banking businesses, introducing new channels and interconnections within the banking system; this evolution underscores the changing dynamics of a financial industry driven by technology.

Navigating the risks

Strategic Risks

Strategic risks emerge from the threats posed to a bank’s business strategy due to digitalisation. Banks must adapt to evolving customer preferences, competitive pressures, and technological advancements. Continuously evaluating and adjusting strategies is vital to remain in sync with the digital transformation sweeping through the financial sector.

How can banks adapt?

By investing in agile technology platforms that allow for rapid adjustments to shifting market demands and customer behaviours.

Reputational risks

Reputational risks arise from operational mishaps, regulatory non-compliance, or adverse public perception. The use of advanced technologies like AI and ML can result in unfair outcomes, tarnishing a bank’s reputation. Collaborations with non-bank entities also carry risks if problems occur[6]. Upholding trust requires clear communication, transparency, and adherence to ethical standards.

How can banks adapt?

By implementing AI ethics committees to oversee the fairness and transparency of their AI/ML systems, and conducting appropriate due diligence on their collaborators and external service providers.

Operational risks

Operational risks encompass internal failures, external events, or flawed processes. Digitalisation heightens complexity and reliance on technology, which can increase the likelihood of operational issues. Strong risk management practices and internal controls are crucial to mitigate these risks and ensure technological robustness.

How can banks adapt?

By conducting regular cybersecurity drills and updating their internal control systems to handle new technological challenges.

Data issues and related risks

Data-related risks involve challenges in data governance, privacy, security, and compliance. Effective data management is essential for protecting customer information and meeting regulatory requirements. Banks need to implement robust data governance frameworks and security measures to prevent data breaches and misuse.

How can banks adapt?

by adopting advanced encryption methods and regularly auditing their data governance protocols to ensure compliance.

Financial stability risks

Digitalisation introduces systemic risks that may affect financial stability. Greater interconnections with fintechs and tech firms add to the complexity. Rapid technological scaling can expose systemic vulnerabilities. Regulators must monitor and manage these risks to maintain the financial system’s resilience.

How can banks adapt?

By collaborating with regulators to develop frameworks that address the complexities introduced by fintech partnerships and technological innovations.

Conclusion

The digitalisation of finance, driven by cutting-edge technologies like AI, ML, DLT, and cloud computing, opens up a world of unprecedented opportunities for banks while also presenting significant risks. To stay ahead in this dynamic landscape and meet the ever-evolving customer preferences, banks must continuously innovate and adapt their strategies. Embracing effective governance, robust risk management, and comprehensive data governance frameworks is essential to prevent operational failures, data breaches, and regulatory non-compliance.

As digitalisation increases interconnections within the financial system, systemic risks emerge, demanding vigilant oversight and flexible regulatory frameworks. For banks and regulators, working together is vital to foster responsible innovation and ensure financial stability. By skillfully balancing innovation with strategic risk management, banks can master the digital transformation, seize new opportunities, and strengthen their resilience.

To learn more about how AI, ML, DLT, and cloud computing are shaping the future of finance and explore our dynamic startup ecosystem, visit the LHoFT website. Discover the resources and opportunities we offer to support your journey in the digital financial landscape.

Featured image source : Midjourney

[1] Regulation (EU) 2022/2554 of the European Parliament and of the Council of 14 December 2022 on digital operational resilience for the financial sector and amending Regulations (EC) No 1060/2009, (EU) No 648/2012, (EU) No 600/2014, (EU) No 909/2014 and (EU) 2016/1011 https://eur-lex.europa.eu/legal-content/en/TXT/?uri=CELEX:32022R2554

[2] https://www.bis.org/bcbs/publ/d575.htm

[3] See “Distributed ledger technology in payment, clearing and settlement – an analytical framework” (27 February 2017) https://www.bis.org/cpmi/publ/d157.htm

[4] https://www.americanbanker.com/payments/news/jpmorgan-details-its-invisible-role-with-amazon-and-others

[5] https://www.apple.com/apple-card/

[6] See the case of JPMorgan against Fintech startup Frank: https://www.fastcompany.com/90834226/jpmorgan-chase-frank-closed-student-aid-startup-fake-users