AML: A Vital Element to Ensuring Financial Stability in Europe

In the words of the European Parliament, even after five different regulations spread into thirty years, money laundering and the related financing of terrorism and organized crime remain significant problems at Union level, thus “damaging the integrity, stability and reputation of the financial sector and threatening the internal market and the internal security of the Union.” The fight against money laundering and terrorist financing is seen as the vital element to ensuring financial stability and security in Europe.

The most recent scandals revealed the extent of the ongoing money laundering problem. Major European banks were exposed as corruption havens, involved in cross-border money laundering scandals, and sitting on top of tax frauds in the past months. The eased cross-border market rules, which were initially created to enable a common market standard, seem to be enjoyed more by criminals rather than the initial target: entrepreneurs and ordinary citizens. AML audits result in increasing penalties for credit institutions, turning the whole process into a vicious cycle.

EUROPOL states that the scale of money laundering is difficult to assess but is nevertheless significant. According to the United Nations Office on Drugs and Crime, the estimated amount of money laundered globally in one year is 2 – 5% of global GDP, which has a noteworthy economic impact from top to bottom. Sanction Scanner’s research indicates that the total amount of AML fines has almost doubled every year globally since 2018.

According to Comply Advantage, since 2002, European authorities issue the most anti-money laundering fines Following the US and the UK. Having all necessary regulations and supervision mechanisms in place, Europe has not been able to create the preventive effect, and the situation calls for immediate action.

Why does the current regulatory framework not suffice? The words of Andrea Enria, The European Banking Authority (EBA)’s former chairman and the current Chair of the Supervisory Board of the European Central Bank (ECB), offer an explanation to the little success of the existing regulations “If you are in the single market, the strength of anti-money laundering controls can only be as high as the weakest link. So if you have a weak authority, then the criminal money may enter the single market.” So, unless the rules are harmonized, and supervision is centralized, no rule is not robust enough to prevent the corruption of the financial institutions in the Union.

Back to Basics: How Does Money Laundering Occur?

The Financial Action Task Force (FATF), the global money laundering and terrorist financing watchdog, defines money laundering as the processing of these criminal proceeds to disguise their illegal origin. The crime is mostly associated with financial institutions and banks, but in reality, the money laundering act is older than banks. Although the term “money laundering” is rumored to have originated in Italy around the 1920s, the first-ever money laundering activities were recorded to be carried out by Chinese bureaucrats 2000 years ago, to hide income from the government. The act and the methods have evolved ever since, but the goal remains to be the same.

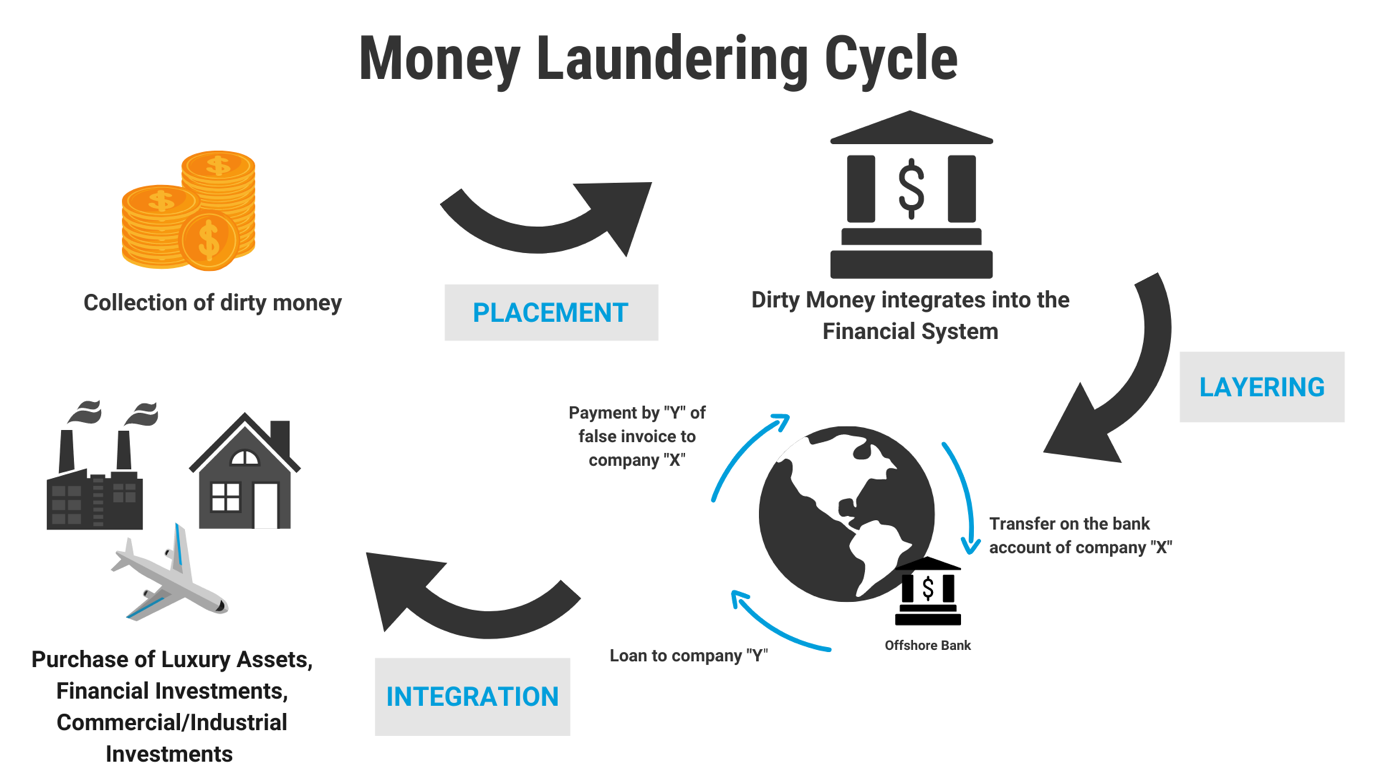

The typical money laundering process involves three stages, namely, placement, layering, and integration. In the placement stage, the criminal gains enter the financial system, using complicated illegal methods. In the next step, the illicit money gets mixed with legitimate funds, i.e., the layering stage. No matter what channel is used during this stage (gambling, investments, business transactions), the goal remains to make it hard to differentiate the funds’ origins. The last stage, integration, completes the money laundering cycle and integrates the illicit money into the legitimate economy.

Source: http://www.unodc.org/unodc/en/money-laundering/laundrycycle.html

Casinos, shell companies, and all sorts of credit and financial institutions are the most significant institutions abused for money laundering. That’s why all professions and institutions handling /channeling transactions are required to apply due diligence transactions to their customers and are singled out by the existing regulations.

The European Approach

Europe has a preventive approach to money laundering. Entering into force in 1991, the First AML Directive ((91/308/EEC) provided the initial anti-money laundering and terrorism financing prevention framework, requiring institutions to perform due diligence on potential customers and beneficiaries and to monitor relationships, assess risks, and report. The Directive brought in some minimum requirements, which were amended and updated in the following versions.

Over the following thirty years, there were subsequent regulations that aimed at fine tuning the European framework and updating it according to market needs and technology developments. Regardless, Europe’s fight against money laundering and terrorist financing continued, since the existing regulatory framework was not able to reduce the burden.

The most recently updated regulation, AMLD4 (Directive (EU) 2015/849), passed in May 2015, foreseeing an implementation deadline of June 26, 2017. Incorporating FATF recommendations into European practice, AMLD4 increased the scope of application, ensuring accountability and transparency.

AMLD4 was definitely stricter than its predecessor. However, it did not create the preventive effect Europe needed, especially due to the new players’ entrance to the financial system and the new technologies and tools criminals started using. According to the EC, the Panama Papers incident as well as the terrorist attacks revealed that complex ownership structures have been used to hide links to criminal activities and tax obligations. All these developments triggered the urgent need for an updated AML Directive, AMLD5 (Directive (EU) 2018/843), that recognized the new tools and methods (e.g., cryptocurrencies) used by the criminals.

AMLD5 entered into force on 19 June 2018, extending the scope to virtual currency providers, art worker traders, e-wallet providers, and tax-related services, aiming to reveal the beneficial owners of more companies, trusts and other corporate vehicles.

Fast forwarding to 2019, the dust didn’t seem to settle even after extended regulations. After months of debate on the sufficiency of the existing regulations, on July 24th, 2019, the European Commission released a report to the European Parliament and the Council, assessing the vulnerabilities of the existing regulatory framework. The report identified four broad categories under which shortcomings of the existing regulations may be grouped:

1) ineffective or lack of compliance with the legal requirements for anti-money laundering/countering the financing of terrorism systems and controls,

2) the governance failures in relation to anti-money laundering/countering the financing of terrorism,

3) the misalignments between risk appetite and risk management, and

4) the negligence of group anti-money laundering/countering the financing of terrorism policies.

The report’s findings were considered an open call for a regulatory reformation, upon which the Member States agreed to create a single rulebook (November 2020).

To create an even more structured supervisory approach, EU banking regulators started looking more closely at the implementation of the anti-money laundering prevention directives, beginning with the Sixth Anti-Money Laundering Directive (AMLD6), Directive (EU) 2018/1673, and planned to be spread over the next couple of months.

AMLD6: What’s New?

AMLD6 is the latest revision of the EU AML regulations, and European credit institutions’ fight against financial crimes will take a whole new turn with the compliance deadline of June 3rd, 2021.

Following the footsteps of its predecessor AMLD5, the regulation which introduced cryptocurrency into the world of finance, ALMD6 aims to harmonize the AML regulations beyond loopholes.

- First and foremost, AMLD6 harmonizes the definition of money laundering crime. The Directive includes a list of 22 predicate offences across the Member States, including cybercrimes and environmental crimes. This approach ensures that these 22 predicate offenses will be criminalized across the Union, regardless if they were defined as a criminal act under the domestic penal codes or not.

- AMLD6 additionally defines the following activities punishable as a criminal offence under the scope of money laundering:

(a) the conversion or transfer of property, knowing that such property is derived from criminal activity, for the purpose of concealing or disguising the illicit origin of the property or of assisting any person who is involved in the commission of such an activity to evade the legal consequences of that person’s action;

(b) the concealment or disguise of the true nature, source, location, disposition, movement, rights with respect to, or ownership of, property, knowing that such property is derived from criminal activity;

(c) the acquisition, possession, or use of property, knowing at the time of receipt that such property was derived from criminal activity.

- The Directive broadens the definition of the illicit act, including aiding and abetting, inciting, and attempting under the scope. This update puts the “enablers” under a whole new light.

- Another significant change is the extension of criminal liability to both legal entities and natural persons holding a “leading position” in the legal entity that commits crime. The changes hold legal entities accountable for money laundering acts and triggers a wide catalogue of punishments.

- The minimum prison sentence for money laundering crimes is increased to four years.

- Under the new rules, multinational companies can finally benefit from a single European standard, a real harmonization if you will, instead of different rules for every different country they operate in.

- Last but not least, AMLD6 addresses the issue of dual criminality, especially in terms of information sharing between jurisdictions.

All in all, the Sixth Directive applies to a number of obliged entities, namely credit institutions and other financial institutions, payment institutions, a number of “vulnerable” professions including lawyers, notaries, real estate agents, providers of gambling services and the services that include transfer of large amounts of cash (EUR 10k). As a rule of thumb, all companies and professions owning customer relationships are affected by the regulation.

The Member States have only a couple of months before the compliance deadline. In the meantime, obligated entities are encouraged to strengthen their AML and compliance teams, re-structure their daily operations, including KYC, KYB, and due diligence processes. To avoid potential liability, they will need to re-establish their internal and external risk scoring processes and filter the processes and the team for weaknesses. They will need to establish enhanced training sessions for their team and understand how to utilize technology (RegTech) to their advantage. There is a lot to do and since the fight against money laundering and terrorist financing is considered to be more critical in the times of coronavirus than ever before, the compliance deadline for AMLD6 is likely to create an even more immense pressure for obligated entities.

Member State Integration and Challenges

The compliance deadline for the Sixth AML Directives is just a few months away, which proves to be a particularly challenging task, as most member states still seem to be between the transposition process of the Fourth and the Fifth Directive. Despite this, The Commission has recently sent letters of formal notice to Germany, Portugal, and Romania for incorrectly transposing the 4th Anti-Money Laundering Directive, which had a transposition deadline of June 2017.

Although the fight against money laundering and terrorist financing is significant, it requires harmonization, collaboration, and constant communication among the Member States and financial institutions. This collaboration proves to be more important than ever since cross border transactions are more vulnerable to manipulation, especially in the times of coronavirus and remote working periods.

In the end, the directives that are transposed into national laws will need to be implemented by obligated entities, which will be the real moment of truth. Will all the credit institutions make it? Regardless of their size and capacity, credit institutions and Fintechs are expected to comply with the regulations without exception. However, with so many new regulations in place and on the horizon, it gets harder and harder for obligated financial entities to comply fully and keep up.

What’s Next After AMLD6?

The restructuring of the anti-money laundering practices will not stop at AMLD6. In May 2020, the European Commission published an Action Plan, putting together stricter measures for the following 12 months, removing weak links discovered in the system announced via the Anti-Money Laundering Package of July 2019. Built on six different pillars, the Action Plan aimed to close loopholes at the national level, better identify and mitigate risks with a refined methodology. Updated and refined, this Action Plan is anticipated to form the base for the single AML Rulebook, expected to be presented within Q1 2021. One of the most significant changes expected to be announced via this Rulebook is to shift the focus of the current domestic AML supervisory scope to a Union-wide extent.

Snapshot on Luxembourg

Luxembourg is being very serious in complying with the European anti-money laundering provisions. In this respect, Luxembourg was in 2019, one of the first European countries to make public the UBO register (requiring registered companies to identify their ultimate beneficial owners (UBOs)) required by AMLD4.AMLD4 and AMLD5 have been implemented under Luxembourg law through amendments of the Law of 12 November 2004. Very recently, through a law of 25 February 2021, the Luxembourg legislator further enhanced and polished the Law of 12 November 2004 and the implementation of AMLD4.

AMLD6 will be transposed into national law by the Luxembourg Bill n°7533 of 18 March 2020. Although Luxembourg’s current legislation is already largely in line with the provisions of the AMLD6, the Bill clarifies and amends certain provisions, mainly by extending the repressive framework and provisions relating to money laundering in the Luxembourg criminal code. The Bill should be adopted shortly.

- An extended and unified regime for money-laundering offences

Until now, the characterization of money-laundering offences was defined by reference to a specific list of predicate criminal offences which has been extended over time. The reference to this list has been deleted. Any crime or delict may now constitute a predicate offence.

- A reduced burden of proof for prosecuting authorities

Such change eases the determination of a money-laundering offense for the prosecuting authorities as they no longer need to characterize the underlying predicate offence. The Bill goes even further by specifying that it is no longer necessary for these authorities to establish all factual elements or circumstances (including the identity of the perpetrator) specific to the predicate offence from which the laundered proceeds originate in order for the laundering offence to be characterized, thus affirming the distinct and autonomous nature of the latter.

- Extended prosecution powers for the repression of money laundering offences

In addition, the Bill eases the prosecution of non-Luxembourg residents, committing a money-laundering offence in Luxembourg, by removing the condition of double incrimination in connection with certain severe predicate offences such as participation in an organized criminal group, terrorism, trafficking in human beings, sexual exploitation, etc. In other words, when such predicate offenses are committed, Luxembourg authorities may prosecute the money-laundering offence even when the predicate offence, was committed abroad by a foreigner who is not a Luxembourg resident and even if such predicate offence is not punishable under the legislation of the country where it was committed.

Likewise, it should be noted that the Bill enables customs and excise officials to prosecute money-laundering offences that are committed following the sale of medicinal substances or drugs.

- An extended confiscation of property for money-laundering offences

The Bill also extends the scope of the confiscation of proceeds of crime by providing that such confiscation, which could already be ordered even in the event of acquittal, exemption from punishment, extinction or statute of limitations, may now be applied to the property that was used or intended to commit the offence, even if such property does not belong to the convicted person.

- An increased liability for professionals and legal entities committing money laundering offences

Finally, the Bill introduces provisions aiming at punishing more severely money-laundering offences when committed by obliged entities (i.e. professionals subject to AML obligations such as professionals of the sector, including credit and financial institutions, notaries and other legal professionals when performing certain activities, trust or company service providers, estate agents, providers of gambling services, etc.).

It therefore appears that the transposition of AMLD6 will toughen the repression of money laundering offences in Luxembourg.

Change is only constant when it comes to regulations. AMLD6 is just the start of a comprehensive regulatory restructuring, including many other adjustments across the sector. Check out Deloitte’s interactive regulatory poster to see what more lies ahead for this year.

by S. Elif Kocaoglu Ulbrich, with contributions from Thomas Berger of Allen & Overy